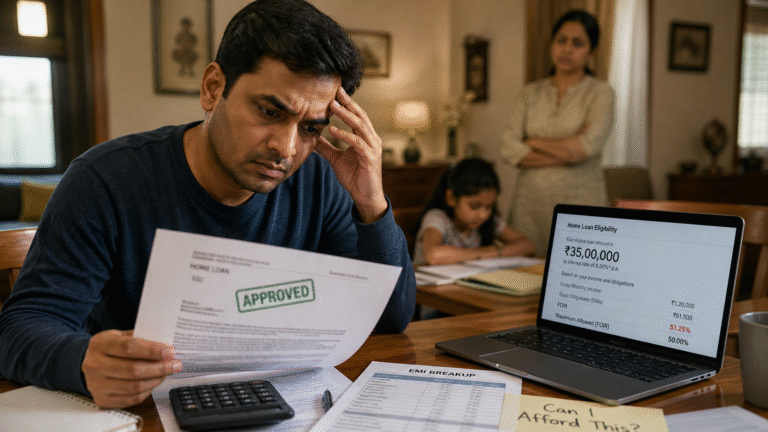

How Home Loan Eligibility Is Calculated in India (Real Formula Banks Use)

Home loan eligibility in India is not calculated based on salary alone. Most people think eligibility = salary.

That’s not how banks actually decide your loan.

☕ Let’s start with something that might feel familiar

You earn well.

You’ve been working for a few years.

You check a home loan calculator—and the number looks promising.

Then you actually apply.

And suddenly, the eligibility is lower than expected.

Or worse… it doesn’t match your plan at all.

That’s when the question hits:

“If my salary is good, why is my loan eligibility lower?”

If you’ve been trying to understand how home loan eligibility is calculated in India, you’re not alone.

Here’s the truth:

Home loan eligibility is not based on salary alone. It’s based on repayment capacity.

Quick Takeaways:

- Eligibility is not based on salary alone

- FOIR is the most important factor

- Higher income ≠ higher loan

- Banks apply hidden filters

🧠 Quick Summary (If You Want the Big Picture First)

- Home loan eligibility depends on repayment capacity, not just income

- FOIR (Fixed Obligations to Income Ratio) is a key deciding factor

- Existing EMIs can significantly reduce your loan amount

- Longer tenure can increase eligibility, but increases interest cost

- Final sanction depends on both income and property value (LTV rules)

How Home Loan Eligibility in India Is Actually Calculated

Banks don’t start with your salary.

They start with a much more important question:

“How much EMI can this person safely pay every month?”

✔ The practical formula lenders use

Eligible EMI = (Allowed FOIR × Monthly Income) − Existing EMIs

Then:

That EMI is converted into a loan amount based on:

- Interest rate

- Loan tenure

This is the backbone of how eligibility works in India. Read our Complete Home Loan Guide to understand the full process.

💸 What Is FOIR and Why It Matters So Much

FOIR stands for Fixed Obligations to Income Ratio.

It tells the lender:

How much of your income is already committed before your home loan even begins.

This is the number that actually decides your loan — not your salary. To understand the safe FOIR limit vs bank FOIR limit in detail, see our dedicated FOIR guide.

✔ Typical FOIR ranges

- 40%–50% → Comfortable

- Up to ~55% → Possible for strong profiles

- Above that → Risk increases

Let’s simplify this with a real example:

✔ Example (simple and real)

You earn ₹1,00,000 per month.

- Existing EMIs: ₹20,000

- Allowed FOIR: 50%

👉 Total allowed obligations = ₹50,000

👉 Available EMI for home loan = ₹30,000

That ₹30,000—not your salary—decides your loan eligibility.

That EMI reduces your eligibility significantly.

💡 Expert Insight

Most borrowers focus on income.

Lenders focus on what remains after obligations.

For a complete breakdown of costs involved, see our guide on Processing Fees & Charges.

Factors Affecting Home Loan Eligibility in India

Home Loan Eligibility in India: Key Factors Banks Consider

- Existing EMIs

- Credit card dues

- Job stability

- Property type

📊 Home Loan Eligibility Based on Salary (Illustrative)

Assumptions:

- No existing EMIs

- Interest rate ~8%

- FOIR at 50%

How Eligibility Changes Based on Salary (Illustration)

| Salary | Max EMI | 20 Years | 25 Years | 30 Years |

|---|---|---|---|---|

| ₹50,000 | ₹25,000 | ~₹25.6L | ~₹29.2L | ~₹34.0L |

| ₹1,00,000 | ₹50,000 | ~₹51.2L | ~₹58.4L | ~₹68.1L |

✔ What this means

- ₹50,000 salary → ~₹25–34 lakh eligibility

- ₹1,00,000 salary → ~₹51–68 lakh eligibility

But actual sanction may be lower due to:

- Existing EMIs

- Credit score

- Age

- Property value

❌ What Most People Get Wrong

Banks don’t use fixed salary multiples

This is not a rule.

It’s just a rough shortcut based on:

- Tenure

- Interest rate

- EMI capacity

Obligations matter more than income

Not always.

Higher obligations = lower eligibility.

When assessing home loan eligibility in India, lenders prioritize how much of your income is already committed to existing obligations — this directly impacts your FOIR.

Eligibility ≠ affordability

No.

Eligibility = what bank is comfortable giving

Affordability = what you should ideally take

🏦 Step-by-Step Example (Clarity Point)

Scenario:

- Salary: ₹50,000

- No EMIs

- FOIR: 50%

- Tenure: 25 years

- Rate: 8%

Step 1: EMI capacity

₹50,000 × 50% = ₹25,000

Step 2: Loan calculation

₹25,000 EMI → ~₹29.2 lakh

Step 3: Real-world filters

- Age

- Property quality

- LTV limits

- Processing fees and charges

Final loan may be lower.

Use our EMI Calculator to estimate your monthly payment before you apply.

🏗️ The Second Filter: LTV (Loan-to-Value)

Even if your income supports a higher loan…

You can’t exceed property-based limits.

✔ RBI LTV guidelines

- Up to ₹30 lakh → up to 90%

- ₹30–75 lakh → up to 80%

- Above ₹75 lakh → up to 75%

According to RBI housing loan guidelines, loan-to-value ratios are regulated based on the property value to ensure responsible lending.

✔ Example

Property value: ₹50 lakh

👉 Max loan ≈ ₹40 lakh

👉 You bring ₹10 lakh

💡 Expert Insight

Your final loan is always:

Lower of income eligibility OR property eligibility

📉 Credit Score: Important, But Not Everything

✔ Typical ranges

- 750+ → Strong

- 700–749 → Acceptable

- 650–699 → Limited options

- Below 650 → Difficult

✔ Reality

Even with a good score:

👉 High EMIs or unstable income can reduce eligibility

🏦 Banks vs NBFCs: Why Results Differ

Banks:

- Lower interest rates

- Stricter rules

- Prefer salaried profiles

NBFCs/HFCs:

- More flexible

- Useful for non-standard profiles

- Slightly higher rates

💡 Insight

Different lenders = different eligibility outcomes.

🧭 A Simple Self-Check Before Applying

Ask yourself:

- Is my income stable?

- Are my EMIs under control?

- Is my credit clean?

- Is the property acceptable?

If yes → smoother approval chances

Before you apply, understand how banks actually assess your loan.

→ Start the Complete Home Loan Guide

Home loan eligibility in India depends on multiple factors beyond income. Understanding how banks calculate eligibility helps you make better borrowing decisions.

🌿 Final Thought

Home loan eligibility is not just a number.

For borrowers navigating home loan eligibility in India, understanding these filters — FOIR, LTV, and credit profile — is what separates a smooth approval from repeated rejection.

It’s a risk-based decision.

Once you understand this:

You stop chasing maximum eligibility

…and start choosing smart, sustainable borrowing

For general lending concepts, see housing finance overview.

Frequently Asked Questions

Q: How is home loan eligibility calculated in India?

A: Banks use FOIR, income, obligations, and risk factors.

Q: Does salary alone decide eligibility?

A: No. Existing EMIs and repayment capacity matter more.