Why Is My Home Loan Rejected Despite Good Salary & CIBIL? Real Reasons Banks Don’t Reveal

A 6-minute read that explains what banks actually evaluate — and what you can do about it.

Table of Contents

☕ Let's start with something that might feel uncomfortably familiar…

You've done everything "right."

Your salary is decent.

Your CIBIL score looks strong.

You've planned your finances carefully.

You apply for a home loan… and then:

"We regret to inform you…"

No clear explanation. No real clarity.

Just confusion.

And one question quietly sitting in your mind:

"What exactly went wrong?"

If you've been trying to understand the real reasons for home loan rejection in India, you're not alone.

Let's unpack that — properly.

🧠 Quick Summary — If You're Short on Time

Here is what you most need to know before reading further:

- Home loan approvals are based on overall risk, not just salary or CIBIL.

- FOIR (existing EMIs) is one of the biggest hidden reasons for rejection.

- Income stability matters more than income size.

- Your bank statement behaviour is closely evaluated.

- Even strong profiles can get rejected due to property-related risks.

🧠 The Real Reasons Why Home Loans Get Rejected in India

Here's the thing.

A home loan isn't approved based on one factor.

Not your salary. Not your credit score. Not even your overall profile in isolation.

It's a combined risk decision.

The bank is not just asking — "Can you pay?"

It's asking — "Will you keep paying… consistently… for the next 15–20 years?"

Let that sink in for a second.

Because that's where the lens changes.

💡 Key Insight

Banks are not evaluating who you are today. They are evaluating who you will be as a borrower for the next 15–20 years. Your income, your discipline, and the property all need to tell a consistent, low-risk story.

🧩 The Simple Framework Banks Actually Use

Strip away all the jargon, and it comes down to three things:

The bank evaluates three things in every application:

- You (the borrower)

- Your cash flow reality

- The property itself

If even one of these feels slightly risky…

👉 the entire application starts weakening.

And that's exactly why two people who look similar on paper can get very different outcomes.

[Insert Image: A simple 3-column visual or infographic showing the three pillars banks evaluate: (1) Borrower Profile, (2) Cash Flow Reality, (3) Property Risk. Each column shows key sub-factors. Clean, minimal design for mobile readability.]

[Alt Text Suggestion: Three pillars of home loan approval in India — borrower, cash flow, and property risk infographic]

👤 1. It's Not Your Salary — It's Your Income Stability

Let's clear one of the biggest misconceptions.

High income does not guarantee loan approval.

Banks don't chase numbers. They look for consistency and predictability.

Think about it like this…

Who feels safer to lend to?

Someone earning ₹1.2 lakh/month steadily for 5 years

OR

Someone earning ₹2 lakh/month but switching jobs frequently?

You already know the answer.

⚠️ Watch Out

If you recently switched jobs or are still in your probation period, most banks will treat your income as "unverifiable" — even if your salary is higher than before. Wait at least 6 months into a new role before applying.

🚩 Where Income-Related Rejections Quietly Happen

These income situations are where rejection quietly happens:

- Frequent job changes

- Recently joined a new job (especially if still on probation)

- Employment gaps

- Income that's difficult to verify

- Businesses with inconsistent cash flow

[Internal Link Opportunity: documents required for home loan — Home Loan Documentation Checklist]

And honestly… this is where most people get surprised.

Because income looks strong — but confidence in that income isn't.

💡 Expert Insight: What Banks Are Really Underwriting

Banks don't underwrite your current income.

They underwrite your future stability of income.

That's the real game.

💸 2. The Real Silent Filter: FOIR (Fixed Obligation to Income Ratio)

[Featured Snippet Optimized Section]

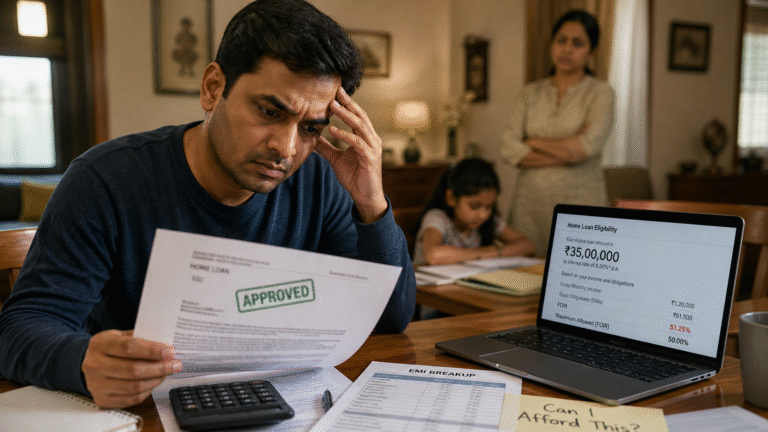

FOIR (Fixed Obligation to Income Ratio) is the single biggest hidden reason for home loan rejection in India.

It measures how much of your monthly income is already committed to existing EMIs and credit card dues.

Most lenders reject or reduce loan amounts when your total obligations exceed 50% of your net monthly income. For a detailed breakdown of the safe FOIR limit and reduction strategies that can help you reapply successfully, see our FOIR guide.

Many people don’t get rejected because they earn less.

They get rejected because too much of their income is already committed.

📊 What Is FOIR and Why It Can Kill Your Application

FOIR = Total Monthly Obligations ÷ Net Monthly Income

Here is a practical example of how FOIR is calculated:

- You earn ₹1 lakh/month

- Existing EMIs: ₹30,000

- Credit card dues: ₹10,000

- 👉 That’s already 40% of income committed — before any home loan EMI is added

Now ask yourself: How much room is left for a new home loan EMI?

Most people say: “Meri salary achhi hai, loan mil jana chahiye.”

Banks think: “Us salary mein se bacha kya hai?”

This is why FOIR matters when calculating how much home loan you can actually get.

[Internal Link Opportunity: how much home loan I can get based on my salary — Home Loan Eligibility Calculator page]

Because eligibility on paper… and affordability in reality… can be very different.

📊 Key Stat

According to industry data, high FOIR is one of the top 3 reasons for home loan rejection in India.

Most lenders flag applications where total EMI obligations exceed 50% of net monthly income.

📊 FOIR Benchmarks Lenders Use

| FOIR Range | Lender View | What It Means for You |

|---|---|---|

| Below 40% | Comfortable | Strong eligibility, good chance of approval |

| 40–50% | Stretch zone | Possible, but may face lower loan amount |

| Above 50% | High risk | Rejection likely; reduce obligations first |

Check Your Home Loan Eligibility Now

Find out if you qualify — get a free eligibility check in minutes.

📉 3. CIBIL Score Helps — But It's Not the Full Picture

A good credit score definitely works in your favour.

But it's not a guarantee.

🔎 What Lenders Look at Beyond Your CIBIL Score

| Credit Factor | How It Hurts Your Application |

|---|---|

| Late payments (even small ones) | Signals payment unreliability to lenders |

| EMI bounces | Direct red flag in bank statement review |

| High credit card utilisation | Suggests cash flow stress |

| Old loan settlements | Treated as partial default by most lenders |

| Loans where you were a guarantor | Counts toward your FOIR and risk profile |

| Closed loans showing as active | Errors that quietly drag down your score |

| Incorrect overdue entries | Must be disputed before applying |

And here's something tricky…

Sometimes, the issue isn't even your fault:

Closed loans still showing as active.

Incorrect overdue entries.

These things quietly impact your application.

💡 Insider Perspective on Credit Reports

[Internal Link Opportunity: how CIBIL score affects home loan approval — CIBIL Score Guide]

Your CIBIL score is just a summary.

Lenders look at the story behind the score.

⚠️ Watch Out

Before you apply for a home loan, pull your free CIBIL report at cibil.com. Errors like "closed loans showing as active" or "incorrect overdue entries" are more common than people realise — and they can silently kill your application.

🏦 4. Your Bank Statement Reveals More Than You Think

This is one area people almost always underestimate.

And honestly… this is where your real financial behaviour shows up.

🔍 What Lenders Observe Closely in Your Bank Statement

Banks observe the following closely in your bank statement:

- Do you maintain a healthy average balance?

- Are your salary or business credits consistent?

- Are there any EMI bounces? (These are direct red flags.)

- Are there sudden unexplained transactions?

☕ Straight Talk on Bank Statement Risk

[Internal Link Opportunity: home loan EMI calculation — EMI Calculator page]

Your bank statement answers one silent question for the lender:

"Can we trust this borrower's financial discipline?"

You can have a good salary and a strong CIBIL score.

But if your bank statement feels messy…

👉 trust takes a hit.

✅ Pro Tip

Before applying, review your last 6 months of bank statements yourself. Look for: EMI bounces, irregular salary credits, and large unexplained withdrawals. Clean up what you can — close dormant accounts, reduce cash-heavy transactions, and ensure salary credits are consistent.

🏗️ 5. Sometimes It's Not You — It's the Property

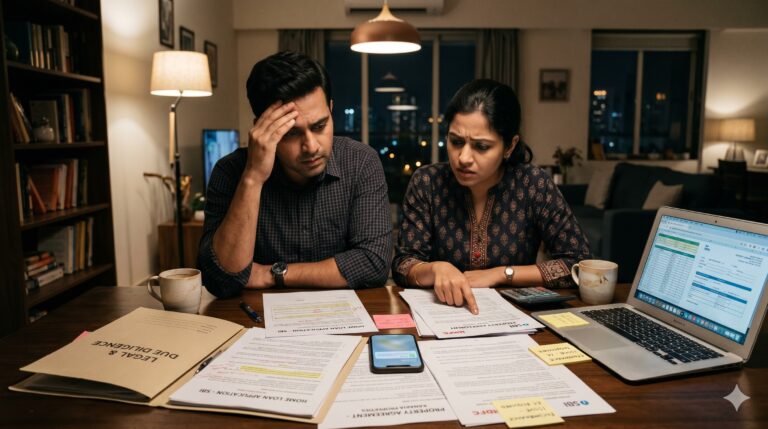

This is where most people get completely blindsided.

You can be perfectly eligible… and still get rejected.

Because the bank is not just evaluating you. It's evaluating the property risk as well.

[Insert Image: A two-column visual showing the two layers of property assessment banks perform: Legal Checks (ownership clarity, title chain, approvals) on the left and Technical Checks (construction quality, plan vs structure, condition) on the right. Below, show how valuation gap affects loan amount.]

[Alt Text Suggestion: Home loan property assessment process in India — legal and technical checks banks perform before approval]

🧾 Legal Checks Banks Run on the Property

The legal checks banks run on the property include:

- Ownership clarity

- Title chain verification

- Required approvals and NOCs

🏠 Technical Checks Banks Run on the Property

The technical checks banks run on the property include:

- Construction quality

- Plan vs. actual structure

- Overall property condition

And then comes valuation…

Banks don't go by your deal price. They do their own independent valuation assessment.

If their valuation is lower:

- Loan amount reduces

- Your contribution requirement increases

- Or the deal falls apart entirely

💡 The Underlying Question Banks Always Ask About Property

"If something goes wrong… can we safely recover this asset?"

That's the lens every property is evaluated through.

[Internal Link Opportunity: property documents required for home loan — Property Verification Checklist]

💡 Key Insight

A borrower can be 100% eligible — and still get rejected because of the property. Banks finance properties, not just people. Always verify the legal and technical status of the property before submitting your application.

🔍 6. Hidden Factors Most Applicants Never Consider

Even when everything looks fine on the surface, these things matter:

| Hidden Factor | Why Banks Consider It |

|---|---|

| Employer profile and reputation | Top-tier employers signal job stability |

| Industry stability | Volatile industries mean income uncertainty |

| Property location | Affects recovery value if loan defaults |

| Co-applicant's financial behaviour | Joint liability = joint risk assessment |

| Internal risk models | Each lender has proprietary scoring criteria |

| Loan-to-Value (LTV) limits | Caps how much of property value can be financed |

🤔 Why Two Similar Applicants Get Different Decisions

Two applicants. Same income. Same CIBIL.

Still get different decisions.

Because underwriting is not a checklist.

It's a multi-layered risk judgment.

💡 Key Insight

Two applicants with identical income and CIBIL scores can receive different outcomes from the same bank. Why? Because underwriting is a holistic, multi-layered judgment — not a mechanical checklist. Your employer, your industry, your property location, and even your co-applicant all factor in.

❌ What Most Applicants Get Wrong About Home Loan Approvals

Let's clean up a few common assumptions:

- ❌ "High salary = approval" — Not really. Stability and obligations matter more.

- ❌ "Good CIBIL is enough" — It helps, but it's not sufficient on its own.

- ❌ "Pre-approved loan = guaranteed" — Final approval still depends on property and documentation.

🧭 A Simple Self-Check to Do Before You Apply

Before you apply, just pause for a moment and ask yourself:

- Is my income stable?

- Are my EMIs within a comfortable range?

- Is my credit behaviour clean?

- Does my bank statement reflect financial discipline?

- Is the property legally and technically sound?

[Internal Link Opportunity: home loan application tips for first-time buyers — Home Loan Application Guide]

If 2–3 of these feel shaky…

👉 that's usually where the problem lies.

🌿 Final Thought — A Rejection Is a Signal, Not a Verdict

So if you've faced a rejection earlier, maybe it wasn't as random as it felt at that moment.

A home loan rejection is not the bank saying: "You're not capable."

It's saying: "This particular combination of borrower, finances, and property… doesn't fit our risk comfort."

And once you understand that…

You stop guessing.

You stop taking it personally.

And you start approaching it strategically.

If you’re planning to apply soon, step back and evaluate your profile through this lens first.

It can genuinely make the difference between a smooth approval… and a frustrating rejection.

[Internal Link Opportunity: how to improve home loan eligibility — Home Loan Eligibility Improvement Guide]

❓ Frequently Asked Questions

Can a Home Loan Be Rejected Even With a High CIBIL Score?

Yes. Lenders evaluate income stability, FOIR, bank statements, and property risk — not just credit score.

What Is the Most Common Reason for Home Loan Rejection?

High FOIR (existing EMIs) and unstable income are among the most common reasons.

Does the Property Affect Home Loan Approval?

Absolutely. Legal issues, low valuation, or poor location can lead to rejection even if the borrower is eligible.

| ❌ What Applicants Assume | ✅ What Banks Actually Check |

|---|---|

| High salary guarantees approval | FOIR — how much of that salary is already committed to EMIs |

| 750+ CIBIL score is enough | Full credit report — missed payments, enquiries, credit mix |

| Job title and employer brand matter | Employment stability — how long in current job, any gaps |

| Property price equals loan eligibility | Bank's own valuation, legal title, and location category |

| Co-applicant always improves chances | Co-applicant's own CIBIL and existing liabilities are checked too |

| More documents = stronger application | Consistency across documents — income, ITR, bank statements must align |

| Rejection from one bank means rejection everywhere | Each lender has different policies — NBFCs often have more flexibility |

Ready to Find Out Exactly Why Your Home Loan Was Rejected?

Get a free eligibility assessment — we'll identify the exact rejection factor and show you the fastest path to approval.