How Much Home Loan Can I Afford in India? (Safe Rule)

Most people over-borrow. This guide shows your safe limit.

Last Updated: April 2026

⚡ Quick Answer: How Much Home Loan Can I Afford in India?

If you’re wondering how much home loan you can afford in India, the honest answer isn’t what your bank tells you — it’s what your lifestyle can sustain. Before you borrow, use these four benchmarks as your personal safety check:

- Keep EMI within 25–30% of your take-home income

- Keep total EMIs under 40%

- Keep property value under 6× annual income

- Maintain 6–9 months emergency savings

Banks may approve more. But approval is not the same as comfort.

🏆 Why Trust This Guide?

✔ Based on FOIR/RBI norms | ✔ Reflects SBI, HDFC, ICICI methods | ✔ Helps avoid costly loan mistakes

💥 The Truth Most Home Buyers Realise Too Late

You can get a home loan approved — and still feel financially stretched within a year. It doesn’t happen suddenly. It creeps in.

By the time you realise this, you’re already locked into a 20-year EMI.

First, your investments slow down. Then, your flexibility reduces. And slowly, every financial decision starts revolving around one thing — EMI.

👉 Reality: Banks are solving a different problem. They ask: “Can you repay this loan?” — but you should be asking: “Can I live well with this loan for the next 20 years?”

🧠 Why Most Borrowers Get This Wrong

At some level, we all want reassurance. So when a bank approves a higher loan amount, it feels like validation — like you can afford it. That’s where the trap begins.

Most people believe:

- “If the bank approved it, it must be safe”

- “Salary will grow — I’ll manage later”

- “Long tenure reduces risk”

⚠️ Warning: These are not strategies. They are assumptions — and expensive ones.

If you’re wondering why banks reject loans despite good salary, read this: Why Your Home Loan Gets Rejected

🏦 How Banks Actually Calculate Your Home Loan

At the core of every loan decision is one number: FOIR (Fixed Obligations to Income Ratio). Learn more about FOIR meaning in home loans and how lenders use it. According to the Reserve Bank of India, responsible lending practices require lenders to assess a borrower’s full repayment capacity.

FOIR = Total EMIs ÷ Monthly Income

⚠️ Warning: Banks are comfortable with FOIR of 40–55% — meaning you could be approved for an EMI that takes away half your monthly income. And technically… you would still qualify. Our guide on how banks determine FOIR limits — and what the safe personal threshold actually is — helps you make a smarter borrowing decision.

⚠️ Eligibility vs Affordability (This Changes Everything)

Understanding the difference between home loan eligibility vs affordability is the most important shift in thinking you can make before borrowing.

| Eligibility (Bank View) | Affordability (Your Reality) |

|---|---|

| Can you repay? | Can you live comfortably? |

| Based on FOIR | Based on life expenses |

| Focus on approval | Focus on sustainability |

| Maximises loan | Protects your lifestyle |

💡 Insight: Eligibility is math. Affordability is life. Confusing the two is where most financial stress begins.

🧭 The 30–40–6–9 Rule: Your Personal Home Loan Affordability Framework

Instead of guessing how much home loan you can afford in India, use this structured framework designed not to maximise your loan — but to protect your future.

✅ Rule 1: EMI ≤ 30% of Take-Home Income

Check your safe EMI to salary ratio before you commit. As a general guide:

- Around 25% → safer zone (especially for variable income)

- Around 30% → ideal balance

- Beyond 35% → pressure starts building

It may not feel risky on day one — but over time, this is where strain begins.

✅ Rule 2: Total EMIs ≤ 40%

This includes everything: home loan, car loan, personal loan, credit cards. Think of this as your breathing limit. Cross it, and even small disruptions start feeling heavy.

✅ Rule 3: Property Value ≤ 6× Annual Income

This rule quietly protects you from overbuying. The real pressure often comes not from EMI alone — but from stretching too far just to afford the house.

✅ Rule 4: Emergency Fund = 6–9 Months of Expenses

Without an emergency fund, even a small disruption can force difficult decisions. With it, you stay in control — even through a job change, medical event, or income gap.

👉 Want to know your safe loan amount?

Use the 30–40–6–9 rule above as your guide — or get a personalised estimate instantly.

⚡ A Quick Reality Check (2-Minute Calculation)

If your monthly take-home income is ₹1,50,000:

- Safe EMI → ₹40,000 to ₹45,000

- Total EMI limit → ₹60,000

- Property value → around ₹90 lakh

No complex calculators. No guesswork. Just a clear, safe ceiling.

📊 Real-Life Comparison: Same Income, Very Different Lives

Assumption: 8% rate | 25 years | ₹2 lakh take-home income

| Profile | Loan | EMI | EMI % | Investing | Stress | Outcome |

|---|---|---|---|---|---|---|

| 🔴 Max | ₹1.05 Cr | ₹81K | 40% | Low | High | Trapped |

| 🟡 Smart | ₹78L | ₹60K | 30% | Healthy | Medium | Balanced |

| 🟢 Safe | ₹60L | ₹46K | 23% | Strong | Low | Flexible |

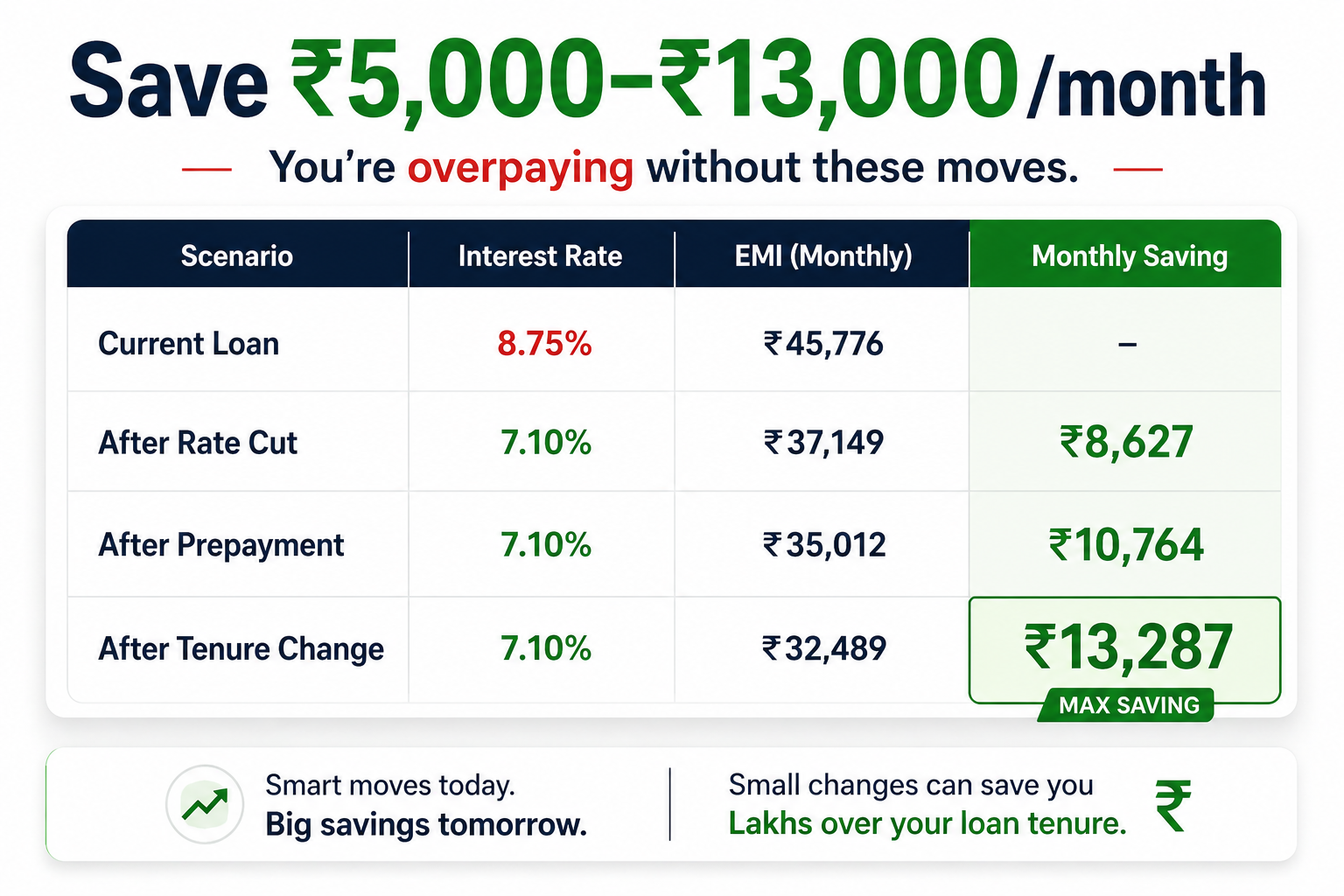

💰 How to Optimise Your Home Loan EMI

Once you know how much home loan you can afford in India, the next step is making sure you’re not overpaying. Small changes — a lower interest rate, a shorter tenure, or strategic prepayments — can save you lakhs over the life of your loan.

🧠 What Actually Happens Over Time

🔴 The Max Borrower

Everything looks fine initially. But within a year, investments slow down, bonuses get mentally allocated to EMI, and financial flexibility disappears. Every expense becomes a negotiation.

🟡 The Smart Borrower

This is where balance shows. The EMI is meaningful — but not suffocating. Investments continue. Prepayments become optional, not urgent. Life moves forward without constant pressure.

🟢 The Conservative Borrower

This path feels slow at first — maybe a smaller home, maybe a delayed upgrade. But financial control stays intact, and upgrades happen later from strength, not pressure.

💡 Insight: The borrower who continues investing often ends up wealthier than the one who stretched early for a bigger home.

📤 The Power of Prepayment

One of the most effective ways to reduce your total loan burden is to make partial prepayments whenever you have surplus income — a bonus, a windfall, or annual savings. Even small prepayments in the early years of your loan can cut your tenure significantly and save lakhs in interest.

💸 The Hidden Costs Nobody Prepares You For

When people calculate affordability, they often stop at EMI. But that’s just the beginning. You also pay for:

- Stamp duty and registration

- Interiors and setup

- Maintenance and society charges

- Insurance premiums

- Moving costs

⚠️ Warning: The real strain often begins not from EMI — but from depleted savings at the point of purchase.

⚠️ The Pre-EMI Trap (Important If Buying Under-Construction)

On paper, pre-EMI looks easy — you pay only interest initially, and the full EMI starts later. But in reality, you may pay rent + pre-EMI together, and the final EMI often comes as a shock. Read our detailed guide on pre-EMI explained before signing any under-construction agreement.

Always evaluate the full EMI upfront — not just the initial comfort of pre-EMI.

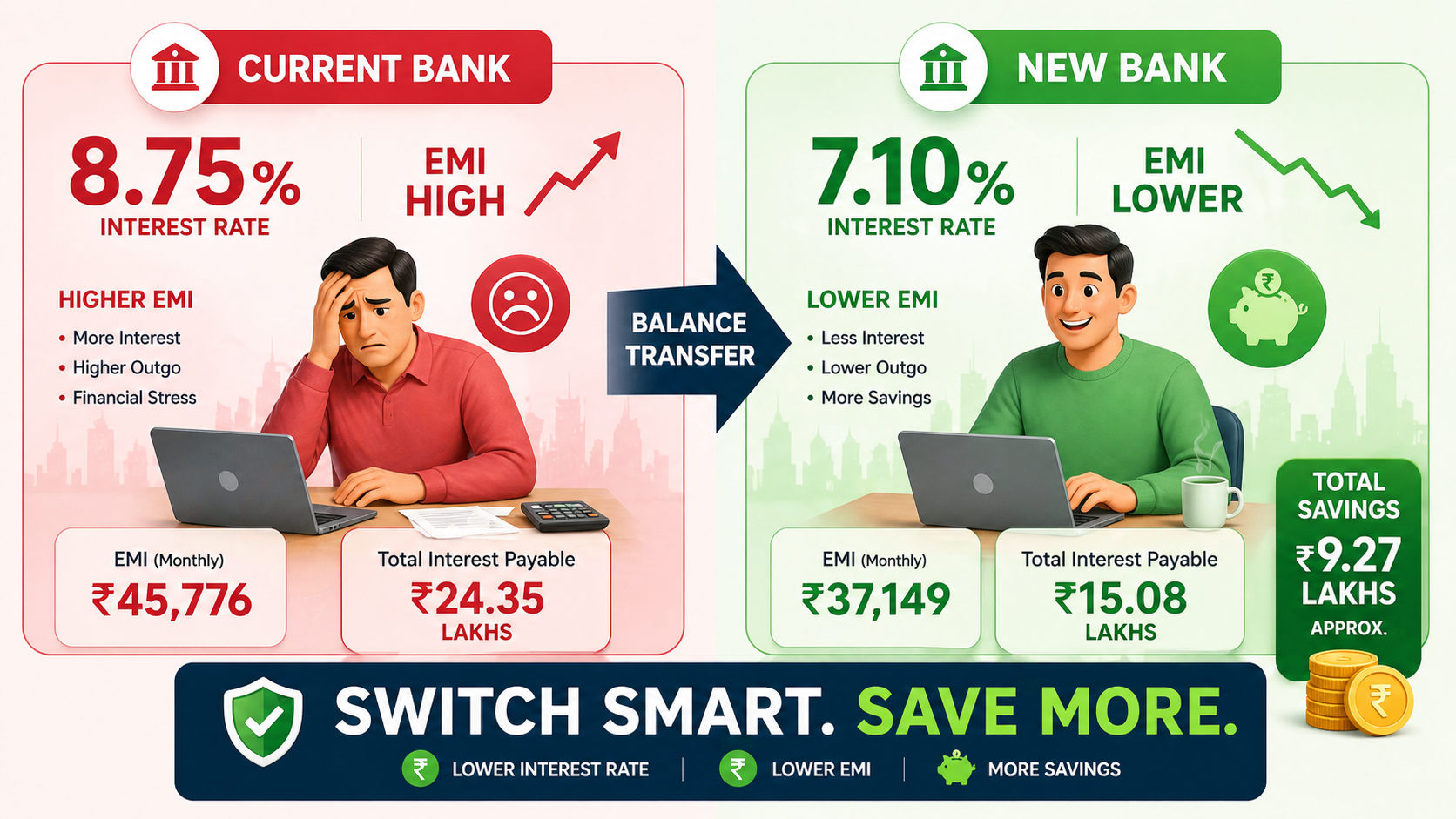

🔄 Should You Consider a Balance Transfer?

If you are already locked into a high-interest home loan, a balance transfer to a lender offering a lower rate can reduce your EMI significantly. This works best in the early-to-mid years of your loan tenure, when interest payments form the bulk of your EMI. Always factor in processing fees and the break-even period before switching.

🧠 What Banks Don’t Optimise For

Banks don’t ignore your future — they simply don’t price it in. They don’t fully account for lifestyle changes, family responsibilities, career risks, or emotional stress. Their job is to ensure repayment. Your job is to ensure freedom and stability.

If you’re also considering improving your loan terms, check how improving your CIBIL score can reduce your EMI burden over the long term.

🎯 Final Decision Trigger

Before you sign anything and finalise how much home loan you can afford in India, pause and ask yourself:

- Will I still be able to invest every month?

- Can I handle 6 months of income disruption?

- Will this EMI control my choices?

If there’s hesitation in any of these answers — you’re likely stretching beyond comfort. You may also want to explore a home loan balance transfer if you’re already locked into a high EMI and want to reduce it.

✅ Final Checklist Before Taking a Home Loan

- Use the 30–40–6–9 rule as your affordability baseline

- Calculate based on take-home income, not gross

- Include all expenses — not just EMI

- Maintain liquidity before and after purchase

- Avoid over-reliance on future income growth

❓ Frequently Asked Questions

❤️ Final Thought

A home loan is not just a financial decision. It shapes your lifestyle, your flexibility, and your future choices. The question of how much home loan you can afford in India is ultimately answered not by your bank — but by your own comfort, goals, and life plan. Choose a loan that fits your life — not just your eligibility.

Disclaimer: This article is for general informational purposes only and does not constitute financial advice. Please consult a qualified financial advisor before making any borrowing decisions.