FOIR in Home Loan India: Safe Limit vs Bank Limit

FOIR in home loan is the single most important number that determines how much loan you’ll get — yet most borrowers never check it. If you’re planning to take a home loan in India, understanding your Fixed Obligation to Income Ratio could be the difference between financial freedom and years of stress. This guide breaks down exactly what FOIR means, how banks calculate it, what the safe limit is, and how you can use it to borrow smartly.

- ✔ Based on practical FOIR underwriting principles

- ✔ Reflects real-world bank & HFC behavior

- ✔ Covers salaried + self-employed borrowers

- ✔ Designed to help avoid EMI stress

What is FOIR in Home Loan? (Simple Definition)

FOIR (Fixed Obligation to Income Ratio) is a percentage that shows how much of your gross monthly income is already committed to paying EMIs and fixed obligations. Banks use this ratio to decide whether you can handle a new home loan EMI on top of your existing commitments.

FOIR Formula:

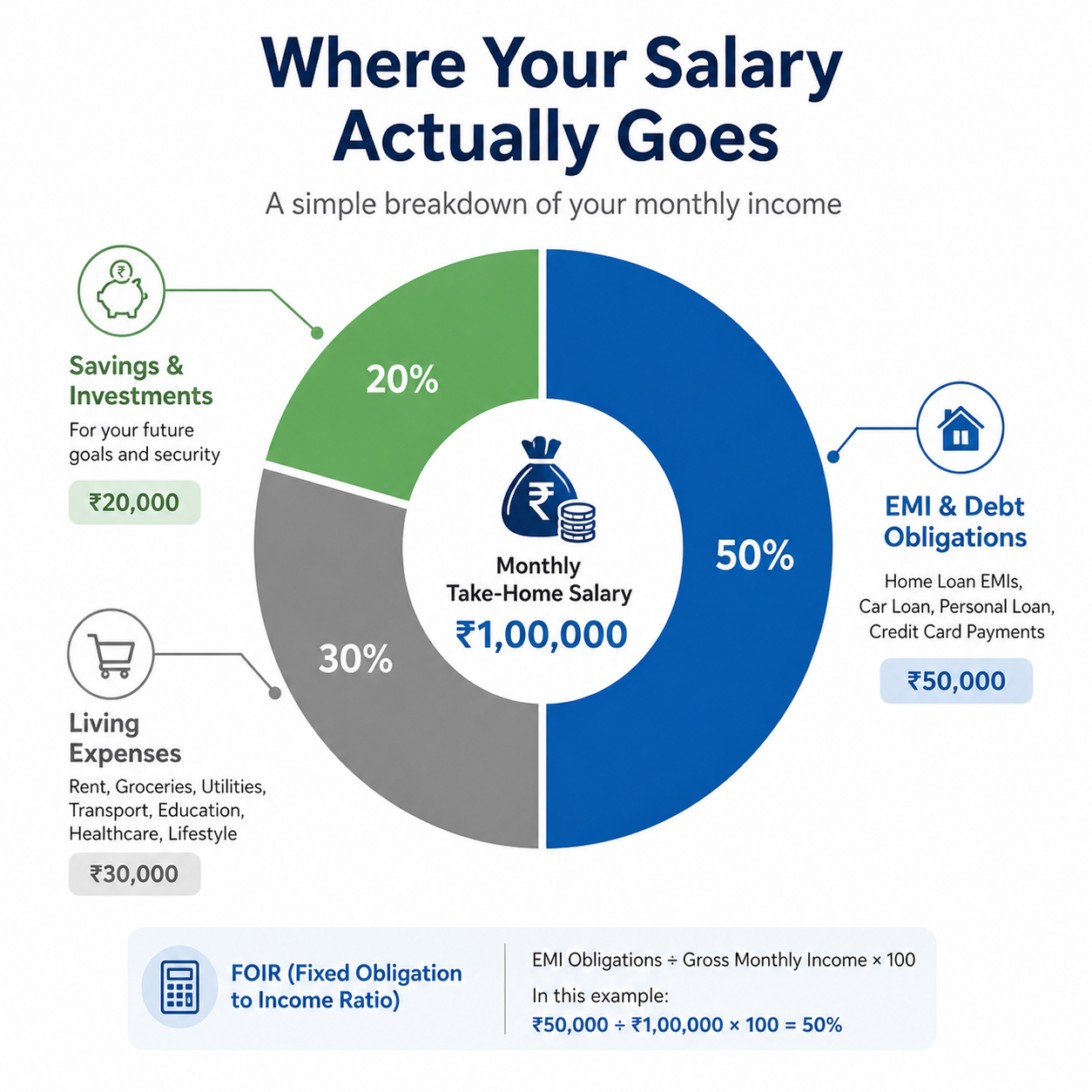

👉 FOIR in home loan = (Total EMIs & Fixed Obligations ÷ Gross Monthly Income) × 100

For example: If your income is ₹1,00,000 and your total EMIs are ₹40,000, your FOIR is 40%.

Under RBI-aligned prudent lending norms, lenders must ensure repayment capacity is reasonable, borrowers are not over-leveraged, and portfolio risk remains controlled. FOIR is one of the core underwriting filters used across banks and HFCs to achieve this.

⚠️ Important: FOIR always includes both your existing EMIs and the proposed home loan EMI. Fixed obligations typically counted include existing EMIs (personal, auto, LAP), credit card minimum dues, consumer durable loans, insurance premiums (select cases), rent (in some underwriting models), and the proposed home loan EMI (mandatory).

💡 Insight: Banks don’t just look at your salary — they calculate your FOIR to understand how much of it is already committed to EMIs. A lower FOIR means more borrowing power and less financial stress.

FOIR vs Eligibility vs Affordability — A Critical Distinction

Most borrowers applying for a FOIR in home loan confuse eligibility with affordability — and this confusion leads to financial stress. Here’s the real difference:

| Parameter | Meaning | Role |

| FOIR | EMI-to-income ratio | Risk control (bank) |

| Eligibility | Max loan you can get | Output of FOIR + LTV |

| Affordability | Comfortable EMI level | Personal decision (you) |

💡 FOIR is designed to reduce default risk — not to maximise your lifestyle comfort. The bank approves what is safe for them. You must decide what is sustainable for you.

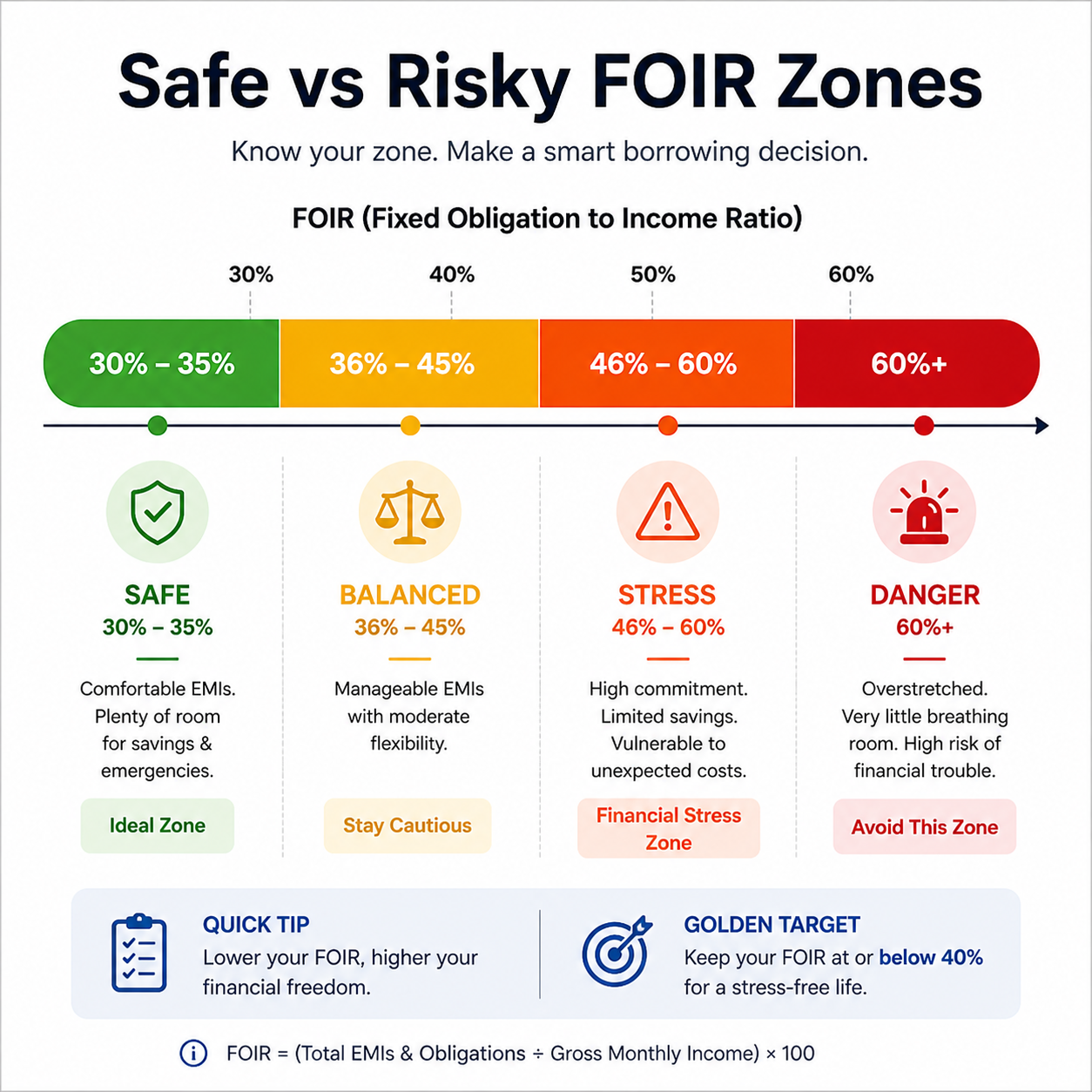

What is a Safe FOIR for Home Loan in India?

The safe FOIR range for home loans in India is generally between 30% and 45%. Here’s how the zones break down:

| FOIR Range | Zone | What It Means |

| 30%–35% | ✅ Safe / Ideal | Comfortable EMIs, strong savings buffer |

| 36%–45% | 🟡 Balanced | Manageable with moderate flexibility |

| 46%–60% | 🟠 Stress Zone | High commitment, limited savings |

| 60%+ | 🔴 Danger Zone | Overstretched, high risk of default |

Most banks in India approve home loans up to 50–55% FOIR for salaried borrowers. However, just because a bank approves it doesn’t mean you should take it. Aim to keep your FOIR at or below 40% for long-term financial health. Learn more about current home loan interest rates to plan your EMI better.

⚠️ Warning: Many borrowers push to the bank’s maximum FOIR limit. That’s the loan they can get — not necessarily the loan they should get. A 55–60% FOIR leaves almost no financial cushion.

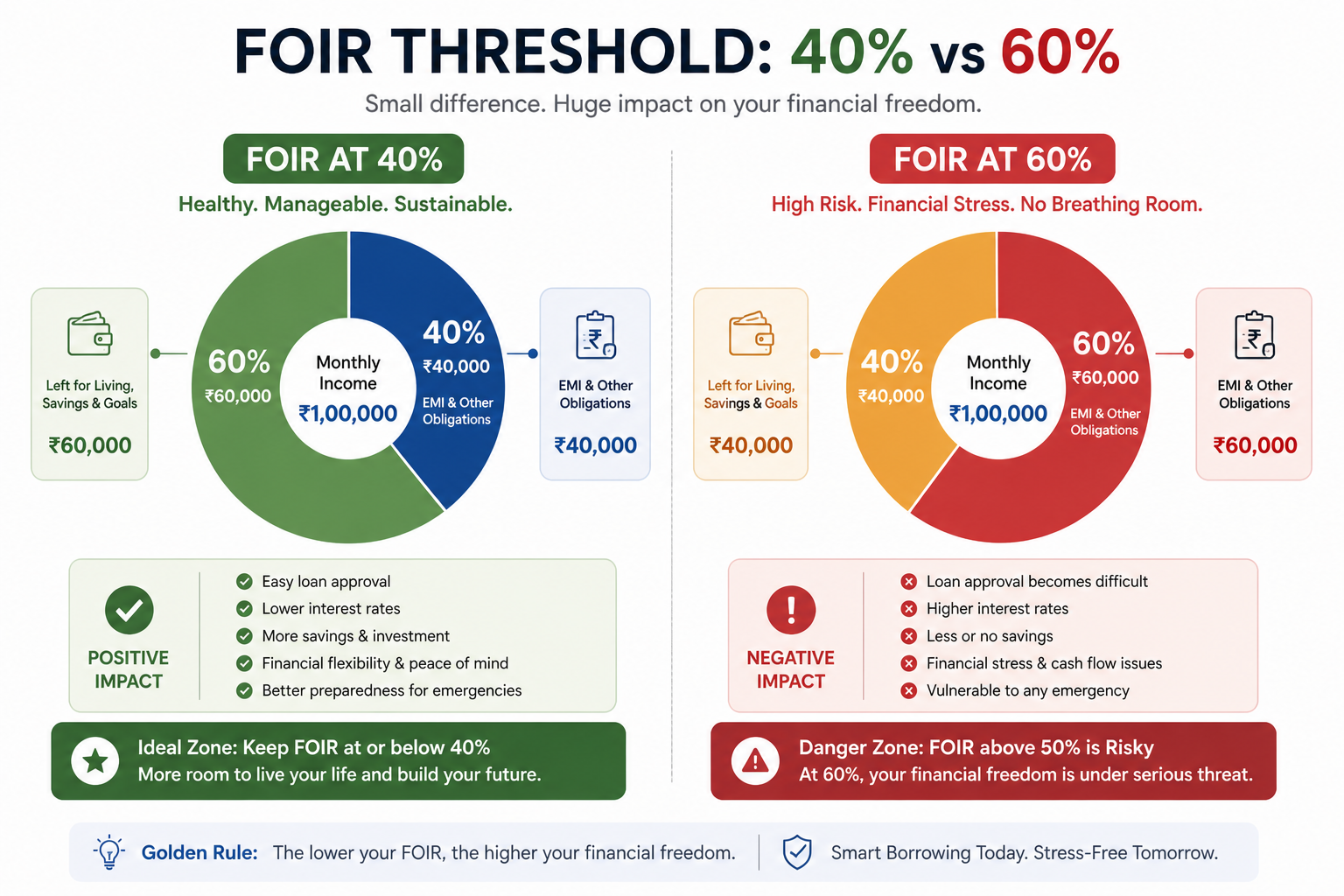

FOIR Calculation Example (₹60,000 Salary)

Let’s say your gross monthly income is ₹60,000 and you have an existing EMI of ₹10,000.

| Scenario | FOIR | Max New EMI | Available for Home Loan EMI |

| At 50% FOIR | 50% | ₹30,000 | ₹20,000 |

| At 40% FOIR | 40% | ₹24,000 | ₹14,000 |

📊 Insight: Higher FOIR increases loan eligibility but reduces savings, emergency buffer, and financial flexibility. A lower FOIR means lower stress and stronger long-term financial stability. Use our free EMI calculator to check your numbers before applying.

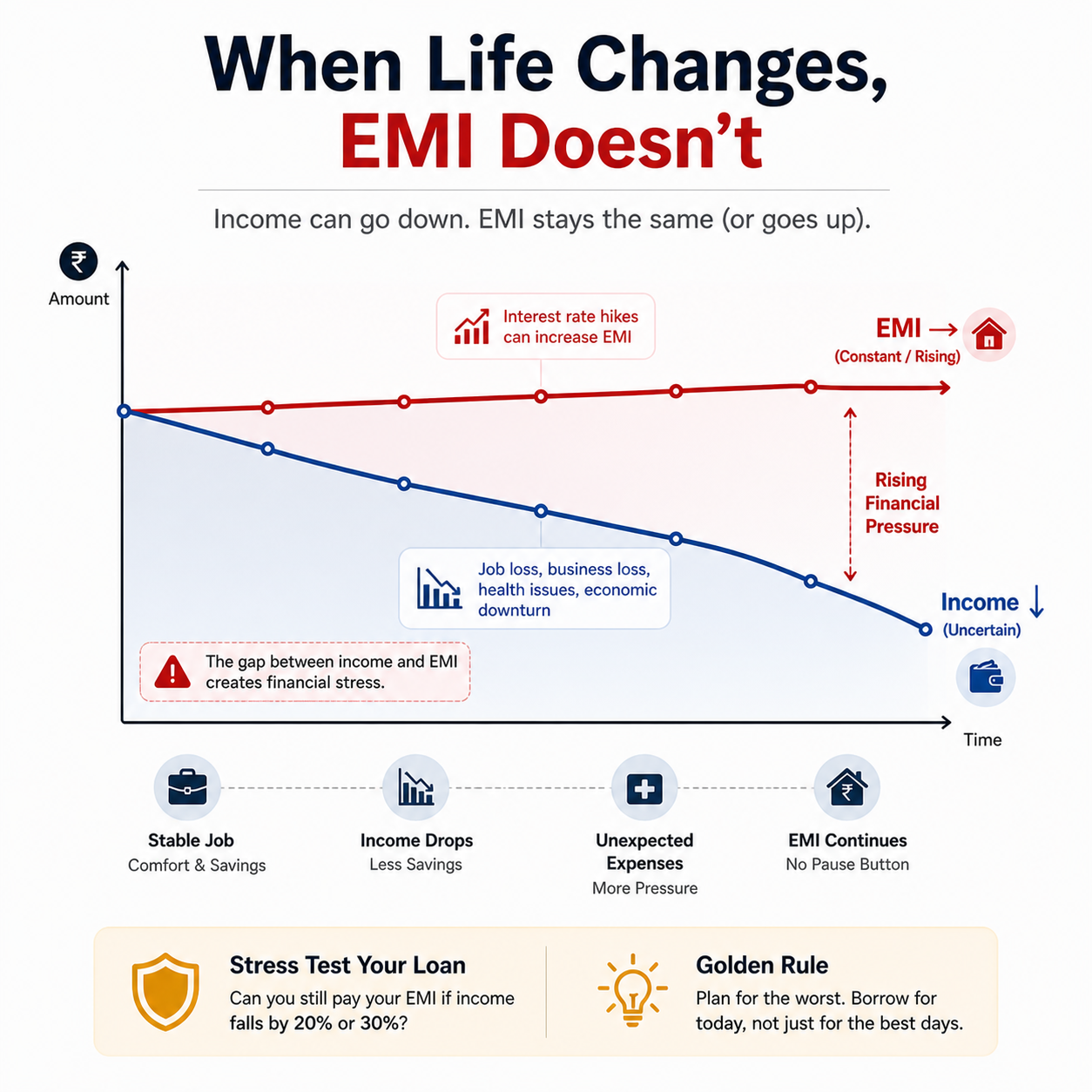

Why a High FOIR in Home Loan Creates Long-Term Risk

One of the biggest mistakes Indian home loan borrowers make is taking a loan that works only under ideal conditions. A high FOIR means you’re already stretched — and any income drop or rate increase can push you into crisis.

Scenario: Income Drops by 20%

| Before | After (Income -20%) |

| FOIR: 50% | FOIR becomes: 62.5% |

| FOIR: 60% | FOIR becomes: 75% |

👉 FOIR problems don’t appear immediately — they appear when income drops or interest rates rise.

👉 Reality Check: Your bank approved your loan at 58% FOIR — then your salary grew by 0% for 3 years. The EMI didn’t change, but everything else got harder. This is how EMI stress begins, not with a missed payment, but with no room to breathe.

4-Step Stress Test Before Taking a Home Loan

Step 1 — Calculate FOIR: (Existing EMIs + Proposed EMI) ÷ Income. Is FOIR ≤ 40%?

Step 2 — Check Savings Buffer: Do you have 6–12 months of expenses saved? If not, build your savings first.

Step 3 — Stress Test: Can you still pay the EMI if income drops by 20–30%? If not, the loan carries high risk.

Step 4 — Final Rule: If your loan only works in ideal conditions, it is risky. A loan should fit your life — not control it.

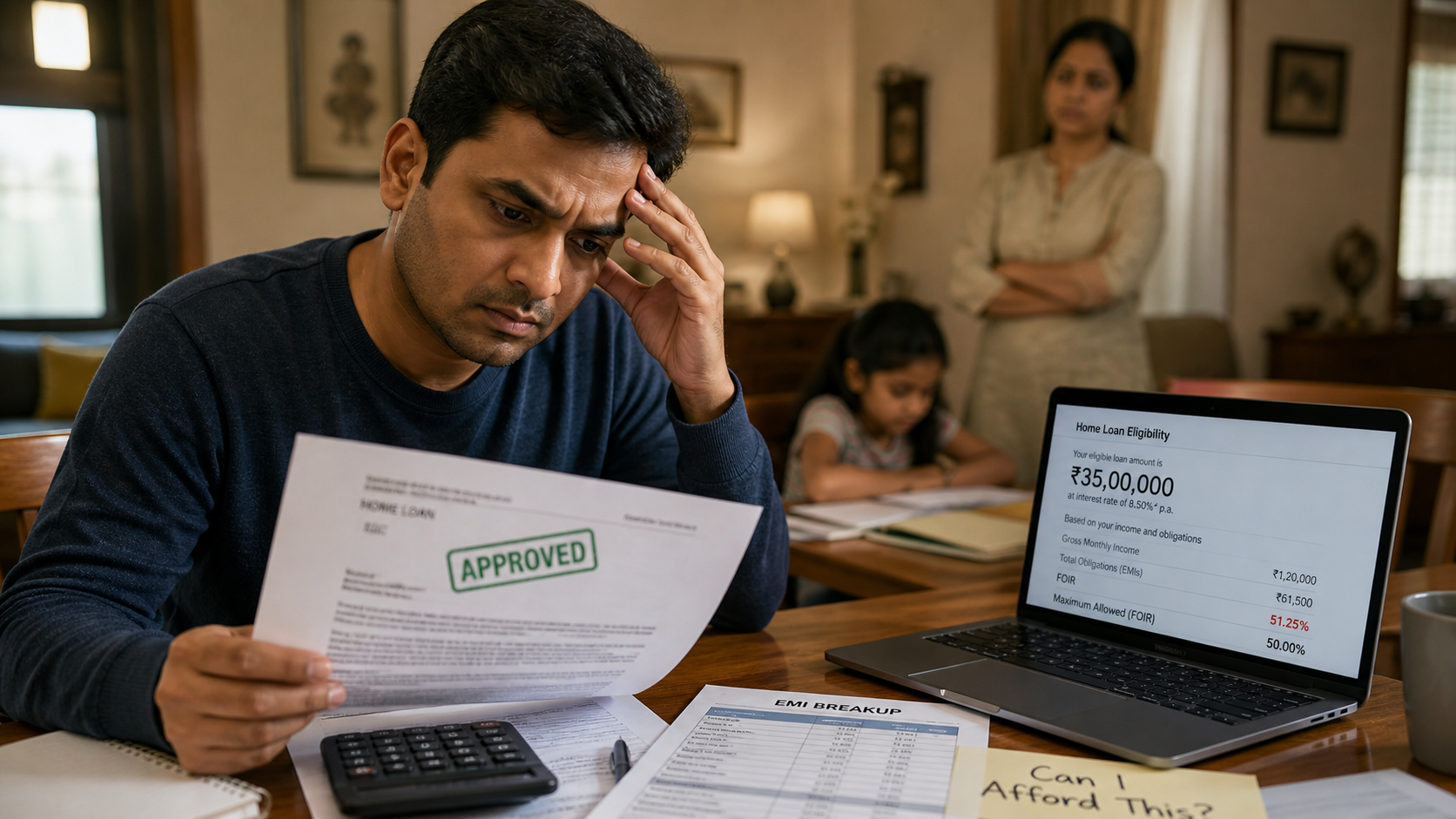

Real Borrower Scenario: When FOIR Looked Fine But Wasn’t

Consider a salaried borrower earning ₹85,000/month who took a home loan of ₹50 lakh with an EMI of ₹42,000 — a FOIR of ~49%. At the time of approval, it seemed manageable.

Two years later: expenses increased, interest rates rose by 1%, and a health emergency wiped out savings. The result? Savings dropped to zero, financial stress increased, and the family struggled every month-end.

💡 Lesson: Loan affordability should be tested across time — not just at approval. Always check what documents and finances you need before committing to a large loan.

How to Reduce FOIR and Improve Home Loan Eligibility

If your FOIR in home loan is too high, here are proven ways to bring it down before applying:

- Close small EMIs first — Clearing personal or car loans before applying reduces your FOIR significantly.

- Add a co-applicant — A working spouse or parent increases combined income, lowering FOIR.

- Increase loan tenure — A longer tenure reduces the monthly EMI amount, improving FOIR.

- Reduce credit card dues — Even minimum dues count as obligations in FOIR calculation.

- Improve declared income — Include all valid income sources such as rent, freelance, or variable pay where accepted.

💡 Strategic Tip: Choosing the right lender matters — different banks allow different FOIR limits. Compare your options using our home loan comparison tool.

FOIR for Salaried vs Self-Employed Borrowers

| Borrower Type | Typical FOIR Limit | Key Considerations |

| Salaried | 50–55% | Stable income, lower risk |

| Self-Employed | 40–50% | Income variability, ITR-based |

Self-employed borrowers face stricter FOIR in home loan assessment due to income variability and cash flow uncertainty. Banks rely heavily on ITR, P&L statements, and banking history for this segment.

💡 Insight: Self-employed borrowers often face stricter FOIR scrutiny. Banks average your income over 2–3 years. If your income fluctuates, keeping your FOIR below 40% gives you a meaningful buffer against assessment risk.

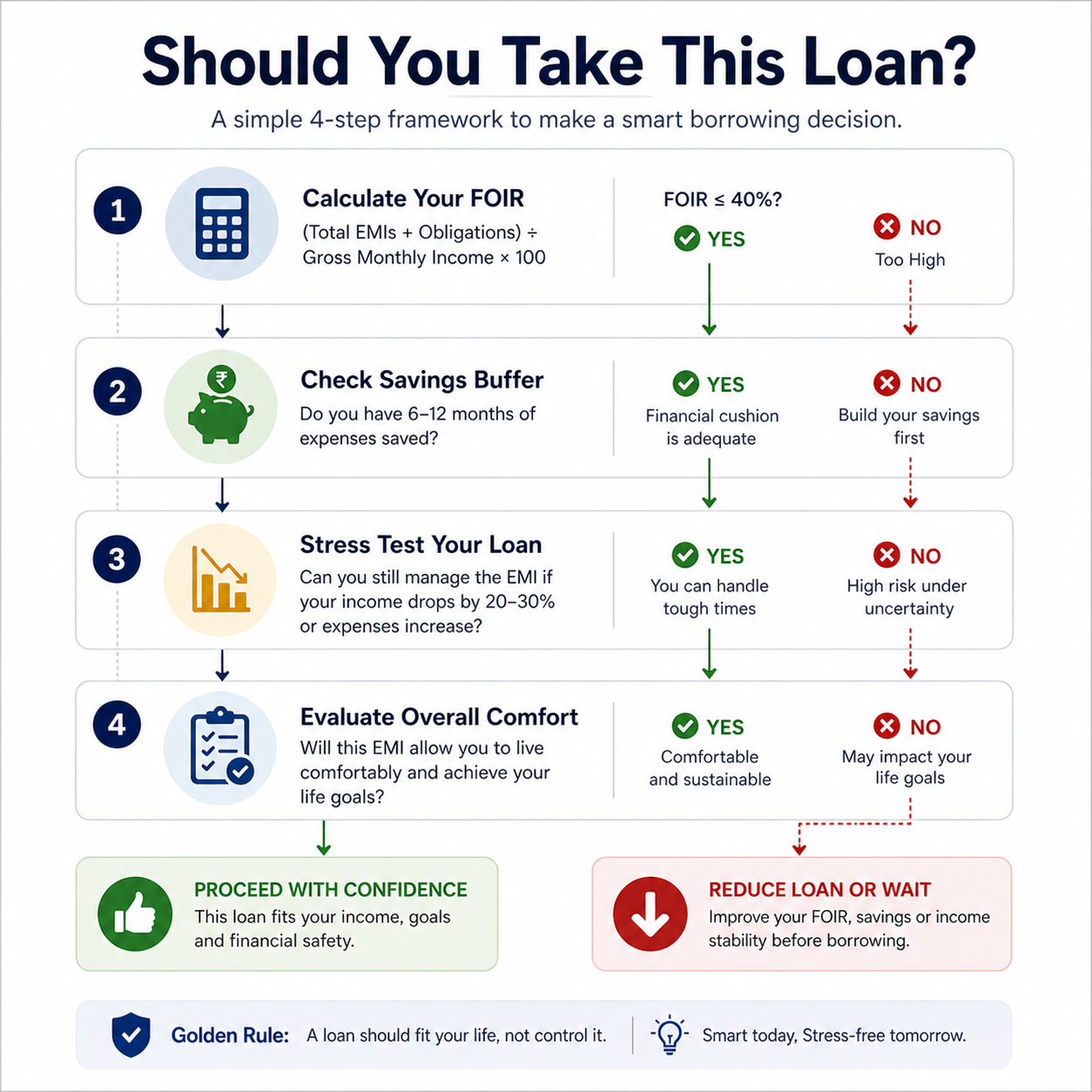

Should You Take This Loan? A 4-Step Decision Framework

Before you sign any loan agreement, run through these four steps:

- Calculate FOIR — Is it ≤ 40%? If yes, proceed. If no (too high), reconsider loan amount.

- Check Savings Buffer — Do you have 6–12 months of expenses saved? If yes, you have a financial cushion. If no, build savings first.

- Stress Test the Loan — Can you still pay the EMI if income drops 20–30%? If yes, you can handle tough times. If no, high risk under uncertainty.

- Evaluate Overall Comfort — Will this EMI allow you to live comfortably and achieve your life goals? If yes, proceed with confidence. If no, reduce the loan amount or wait.

🏆 Golden Rule: A loan should fit your life, not control it. Smart today, stress-free tomorrow.

👉 Want to know your safe home loan limit?

Calculate your affordability before you borrow.

Common FOIR Myths — Busted

| Myth | Reality |

| ❌ Bank approval = Affordability | ✅ Approval = Risk tolerance (bank’s view) |

| ❌ FOIR is standardised across all banks | ✅ FOIR limits vary widely by lender and profile |

| ❌ 50% FOIR is safe | ✅ 50% FOIR is already stretched — aim for 40% |

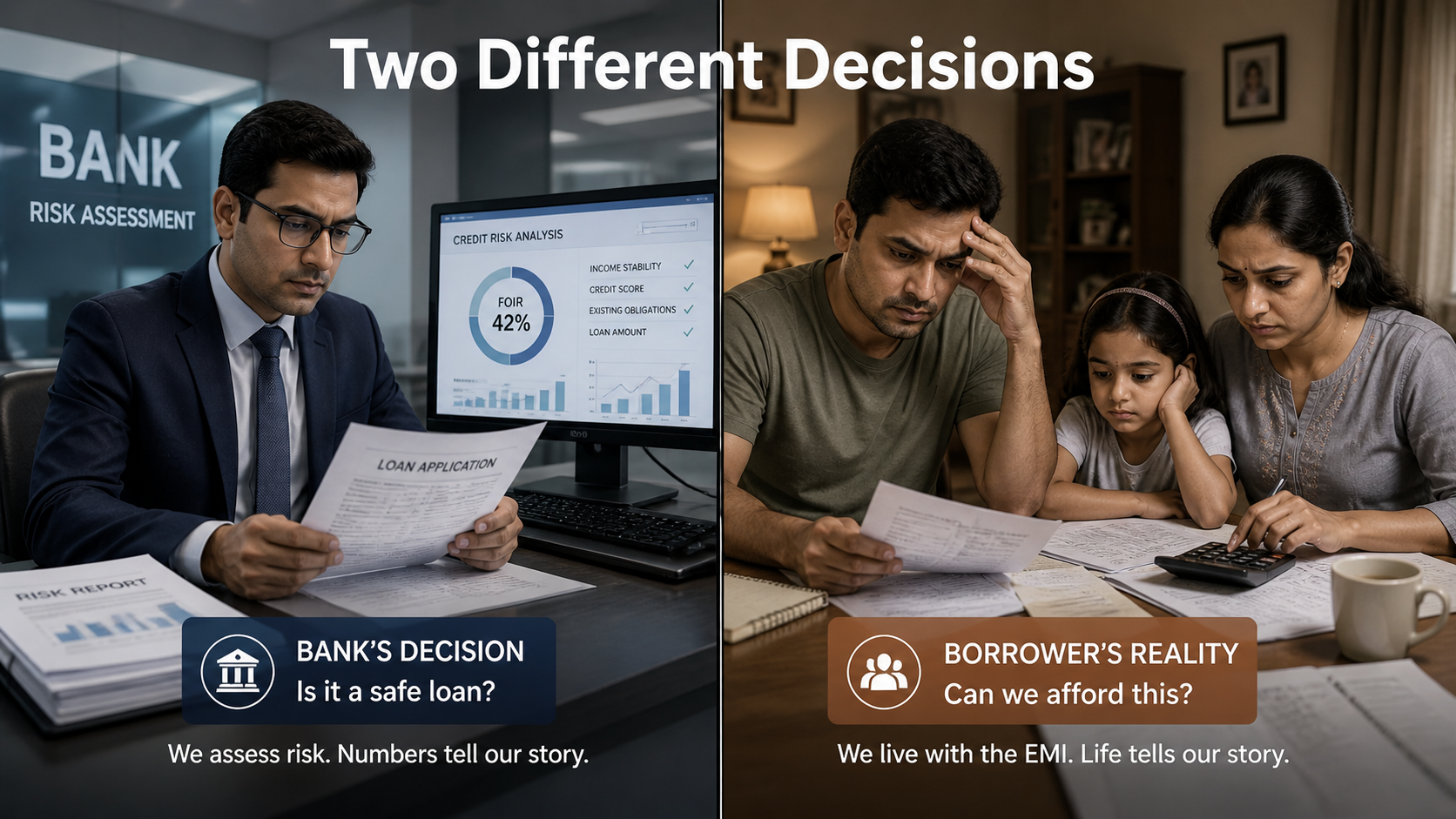

Final Thought: Two Different Decisions

Understanding your FOIR in home loan is not just about getting approved — it’s about building a sustainable financial life. Banks evaluate the probability of default — they want to know if you’ll pay back. You must evaluate the sustainability of your life — whether you can live well while paying back.

These are two different questions. Make sure you’re answering the right one. Check your FOIR, run the stress test, and apply only when your numbers are genuinely comfortable. Read our complete guide on smart home loan borrowing tips before you apply.

Disclaimer: The information provided in this article is for educational purposes only. Please consult a qualified financial advisor before making any borrowing decisions.