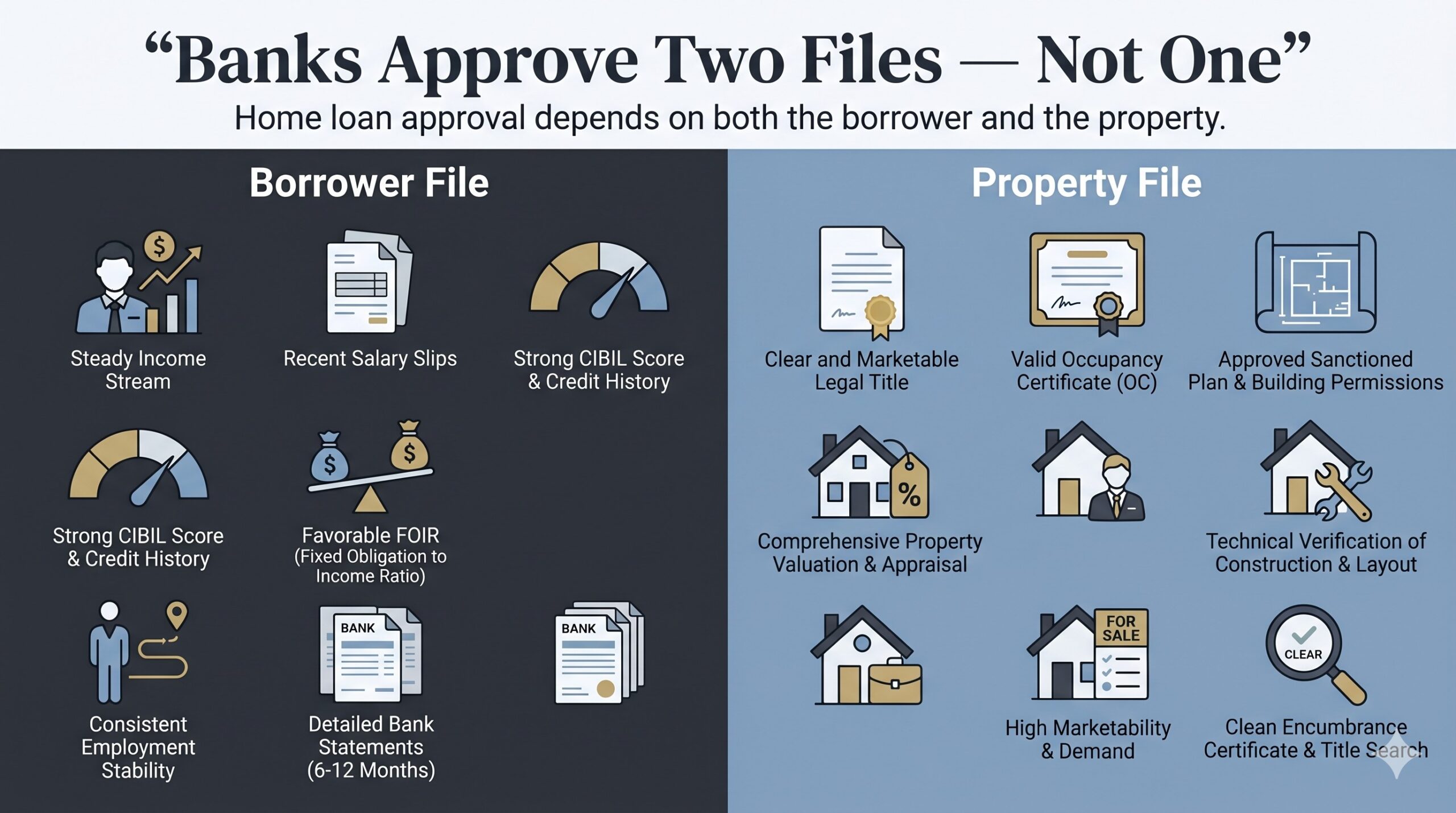

Most borrowers in India never realise this until it’s too late: when you apply for a home loan, the bank doesn’t approve just one file. It approves two. This guide covers everything you need to know about home loan property verification — what banks actually check, and why it matters as much as your credit score.

It approves you — your income, your CIBIL, your FOIR.

And it separately approves the property — its title, its approvals, its valuation, its resaleability.

The property has its own credit file. Its own panel lawyers. Its own valuers. Its own grounds for rejection.

This is why a borrower with a 780 CIBIL and a stable government job can still hear the words “sorry sir, there’s a small issue with the property” two days before registration — and why nobody, not the banker, not the broker, not the builder, will tell them what really went wrong.

Picture the moment. The sanction letter is in the inbox. The family WhatsApp group has already done its rounds of congratulations. The registration date is fixed. The token money has been paid. And somewhere between the legal opinion and the valuation report, the file quietly dies. The front-line response is always vague — “legal team has observation”, “try another bank, sir” — because the actual reason lives in a one-page report the borrower will never get to read.

If you are about to pay token money on a flat you’ve already started imagining your child grow up in, this is the conversation no banker, broker, or builder is incentivised to have with you honestly.

The single most expensive blind spot in Indian home loan decision-making is this: borrowers prepare themselves like a credit file. They forget the property is being prepared too — and graded separately.

The rest of this article fixes that.

Most borrowers don’t discover property-side loan rejection risks until it’s too late. Understanding what lenders assess helps you prepare the right file.

The Silent Rejection: Why Strong Borrowers Lose Loans

Most borrowers walk into a home loan thinking the question is “Will the bank approve me?”

The bank is asking a completely different question: “If this borrower defaults two years from now, can we sell this property quickly, legally, and without litigation?”

Everything else flows from that one sentence.

Banks evaluate two completely separate files: your borrower profile and the property file. A strong borrower profile doesn’t protect you if the property file fails.

A 780 CIBIL doesn’t help if a panel lawyer cannot trace clean ownership across the last 30 years. A ₹3 lakh salary doesn’t help if the valuer reports the building is structurally tired and has no Occupancy Certificate. A government job doesn’t help if the flat sits on Gram Panchayat land that was never converted for residential use.

The borrower’s job is to look financially safe. The property’s job is to look enforceable, legal, and saleable. These are separate examinations, graded independently.

When borrowers get rejected at the property stage, they almost always blame themselves. “Maybe my income wasn’t strong enough.”“Maybe my CIBIL dropped.” It rarely is. In the vast majority of post-sanction rejections we see in India, the borrower’s file was clean. The property’s file was the problem.

Banks don’t just lend to people. They lend against an asset. And that asset gets underwritten as carefully — sometimes more carefully — than you do.

🔍 Underwriter’s Note: Inside a lender, files don’t get rejected by a person — they get coded. A property-led rejection often shows up in internal systems as “asset not financeable” or “legal not clear.” Borrowers hear “try another bank.” The actual reason is buried two layers below the branch.

The earlier you stop thinking like a borrower and start thinking like an underwriter, the more home loan disasters you avoid.

Inside the Underwriter’s Desk: How Lenders Actually Verify Your Property

Most borrowers imagine that a single banker looks at their file and decides yes or no. Inside a bank or HFC, the workflow is far less personal — and far more layered.

Here is what actually happens, in order, once you submit a property to a lender:

1. Basic eligibility screening. Income, CIBIL, FOIR, employment stability. If you clear this layer, you typically get an “in-principle sanction” — sometimes proudly called a sanction letter. This letter feels conclusive. It is not. Read carefully and you’ll see a small but lethal clause: “subject to legal and technical clearance of property.” That clause is where most rejections live.

2. Legal verification. The lender’s panel advocate is briefed. This is not the borrower’s lawyer — it is the bank’s lawyer, paid by the bank, accountable to the bank. The advocate examines the title chain (typically 13 to 30 years), encumbrance certificate, mother deed, mutation records, prior sale deeds, sanctioned plan, OC, CC, RERA registration, and any litigation indicators. The output is a legal opinion that reads one of three ways: clear / clear with conditions / not clear.

3. Technical and valuation verification. A separate empanelled valuer visits the property. They check measurements, construction quality, building age, deviation from sanctioned plan, locality, road width, and comparable market sales. Their job isn’t just to value the property — it is to assess whether the bank can recover its money by selling it later. Their report carries a fair market value and a marketability comment.

4. Credit decision. Only now does a credit officer integrate everything: borrower file + legal opinion + technical report + branch recommendation. The output is one of: sanction at full amount, sanction at reduced LTV, sanction with conditions, or decline.

If any one of these layers — legal or technical — comes back with a serious red flag, the entire loan can collapse regardless of how strong the borrower looks on paper. That is why a 780 CIBIL borrower can lose a deal while a 700 CIBIL borrower in the same building can get one — they bought from different sellers, with different title chains, and only one of them survived legal verification.

🔍 Underwriter’s Note: The sanction letter is not a contract to lend. It is a contract to consider lending, contingent on property checks. Many borrowers treat it as the finish line. Inside the bank, it’s barely the halfway mark.

Most buyers in India never see this system. Your property quietly carries as much weight in your home loan outcome as you do.

The Four Lenses: How Lenders Actually Look at a Property

Underwriters don’t evaluate property through a single test. They run it through four parallel filters. A serious failure on any one of them is enough to break the deal.

Lens

What the lender is really asking

Common red flags

Title

Who legally owns this property, and is that ownership clean and provable?

Broken chain of ownership, missing prior deeds, succession not done, joint owners not signing, GPA-only properties

Approvals

Was this construction legally permitted by the right authority?

No sanctioned plan, wrong jurisdiction approval (DTCP where CMDA applies), unauthorised colony, layout not approved

Technical / Valuation

Is the building physically sound, correctly built, and worth what’s being claimed?

Plan deviations, unauthorised floor, structural fatigue, valuation far below agreement price

Marketability

If we need to enforce and sell this property, can we do it cleanly?

Narrow lane access, redevelopment-prone old building, distress locality, high inventory overhang

A property can be legally clean and still get rejected on marketability. It can be brand new and still fail on approvals (Noida is full of these cases). It can have all clearances and still fail valuation because the seller has overpriced it by 20%.

Each lens runs independently. The deal needs all four to pass.

🔍 What Banks Quietly Notice: Marketability is the lens borrowers underestimate the most. A lender doesn’t just ask “is this property legal?” — it asks “how quickly could we sell this in an auction scenario?” A 30-year-old building on a 15-foot lane in a sparsely traded micro-market can fail this test even with perfect papers. That’s the silent layer no front-line banker discusses out loud.

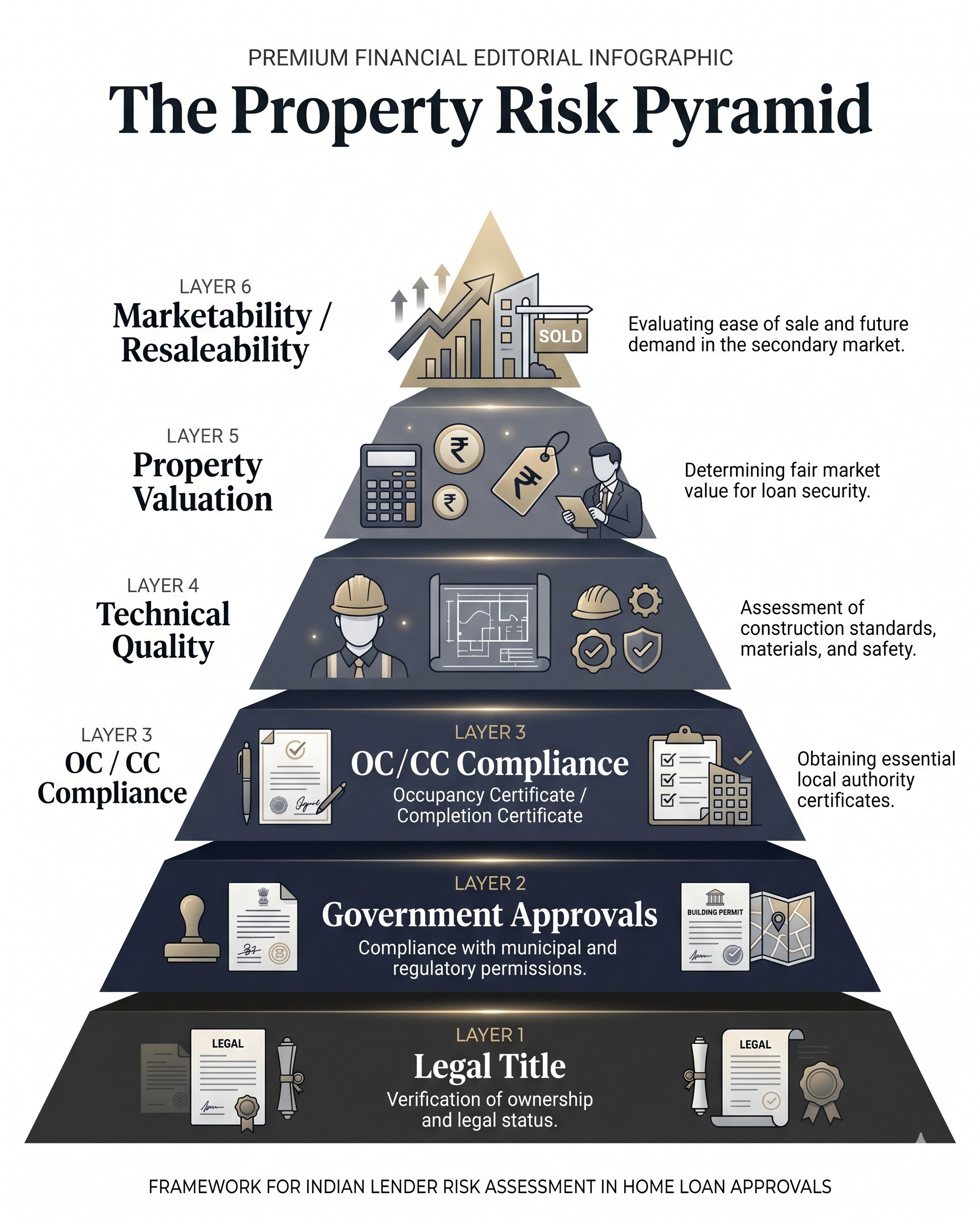

The Property Risk Pyramid: Lenders assess six layers when evaluating a property for home loan security — from legal title at the base to marketability at the top.

📌 Visual placement: insert “The Property Risk Pyramid” diagram here. See visual concept brief at end of article.

Legal Landmines: When Title and Approvals Quietly Kill Your Loan

Of all the ways a property fails underwriting, legal failures are the most frustrating — because the borrower almost never sees them coming. The flat looks fine. The seller has been polite. The broker said “all papers are clear, sir.” And then a one-page legal opinion ends the deal.

What the panel advocate is actually hunting for falls into a few buckets:

Title chain defects. The advocate walks backwards through the property’s ownership history — typically 13 to 30 years depending on the lender. A missing sale deed in 1998. A succession that was never formally registered after a death in the family. A partition between brothers that exists only on a notarised paper, not in any registry. Any of these can be enough to make the legal opinion read not clear.

Existing mortgage or unreleased charge. A surprising number of resale flats in India still carry an old, unreleased mortgage from the seller’s previous home loan — often a defunct HFC or a bank that has since merged. Until that prior lender issues a No Objection Certificate and the charge is formally released, no new lender can safely create its own mortgage. Sellers often genuinely don’t know this; sometimes they do and quietly hope it gets missed.

Succession and inheritance gaps. A flat where the original owner has passed away, the legal heirs haven’t all signed, and the mutation in the society records is still in the deceased person’s name. Banks need clean succession on paper — heirship certificates, registered relinquishment deeds, society transfer — before they will fund the next sale.

Litigation, court cases, encumbrances. Anything pending in court touching the property — a tenant eviction case, a sibling claim, an old service tax notice, a builder vs landowner dispute — shows up on the encumbrance certificate or a litigation search. Many lenders take a hard no-litigation line.

Approval gaps. No sanctioned plan, sanctioned plan substantially deviated from, building completed but no Occupancy Certificate, society conveyance never executed by the builder. In Mumbai specifically, a building without a Society Conveyance Deed creates a layer of risk that conservative banks dislike.

Wrong jurisdiction approvals. This is a Chennai and Bengaluru speciality. A plot approved by DTCP when CMDA applies. A B-Khata property in BBMP limits where the lender wants A-Khata. The property has some approval — just not the right approval.

Legal Issues vs Lender Reaction: The Severity Matrix

Legal issue

Severity

Fixable?

Typical lender reaction

Old unreleased mortgage on title

High

Yes (NOC from prior lender)

Hold disbursal until NOC received

Succession not completed

High

Yes (legal work, weeks–months)

Sanction with condition; cannot disburse without

Title chain broken / missing prior deed

High

Sometimes

Often declined unless deed can be reconstructed

Active litigation on property

Very High

Rarely

Decline

No sanctioned plan / unauthorised construction

Very High

Rarely

Decline

OC/CC missing in completed building

High

Sometimes (regularisation)

Decline or NBFC at lower LTV

Plan deviation (extra floor, illegal extension)

Very High

No

Decline

Wrong authority approval

High

Sometimes

Decline by mainstream banks

Minor NOC missing

Low

Yes

Sanction with condition

The most painful version of this is the clean-looking flat — a polished 2BHK in a respectable society where everything seems normal — that turns out to hide a 22-year-old partition dispute or a never-released mortgage from a defunct HFC. The bank’s lawyer finds it in two hours of records-checking. The borrower had been planning to move in three weeks.

🔍 Underwriter’s Note: Inside lenders, a “not clear” legal opinion isn’t a discussion point. It’s an end point. The branch sales team will tell you “the file got declined” — but the actual cause is a single line in a legal report you’ll never get to read, and the credit officer has no authority to override it.

Technical and Valuation Traps: When the Building Fails the Test

If legal verification is the silent killer, technical and valuation issues are the more public ones — and the more emotionally violent for the buyer, because the rupee figure is staring at them.

A technical verification has two outputs, and both can break the deal:

Output 1: Construction and compliance assessment. Has the building deviated from the sanctioned plan? Is the unauthorised parking floor or terrace room visible? Is the structure showing fatigue inconsistent with the claimed age? Is the construction quality below standard? Is there an obvious access issue — a narrow lane, no clear approach road, encroachment?

Output 2: Fair market value. What is this property actually worth, based on the lender’s internal valuation methodology and comparable transactions? This is the number that controls how much the bank will lend.

The first failure is binary — major deviations or unauthorised construction typically result in a decline. The second failure is more brutal in a different way. The bank doesn’t say no. The bank says yes, but… and quietly shrinks the loan amount.

The Valuation Mismatch Problem

This is one of the most common, most misunderstood, and most expensive surprises in Indian home loan journeys.

What is a valuation mismatch?A valuation mismatch occurs when the bank’s empanelled valuer assesses the fair market value of a property below the agreement value the buyer has committed to the seller. Lenders fund the lower of the two figures, forcing buyers to bridge the gap with margin money.

Imagine a buyer agreeing to ₹1 crore for a flat in an overheated micro-market. They’ve negotiated, paid token, and arrived at the bank with confidence. The valuer visits, reviews comparable sales, factors in age, locality, and market liquidity — and reports a fair market value of ₹85 lakh.

The bank’s policy is rigid: lend on the lower of agreement value vs internal valuation. So instead of funding 80% of ₹1 crore (₹80 lakh), the bank now funds 80% of ₹85 lakh (₹68 lakh). The borrower, who had planned for a margin of ₹20 lakh, now needs ₹32 lakh.

Twelve extra lakh, often at very short notice.

Most borrowers learn this number two days before registration.

What makes the valuation gap dangerous isn’t just the cash shortfall. It is what it signals to the bank’s credit team. A 15% gap between agreement value and bank valuation is the lender’s way of saying the market price is overheated, the locality has weak liquidity, or the property has hidden issues that the buyer is paying a premium for without realising it. In larger valuation deviations, the file often gets re-examined entirely, and some banks decline rather than fund.

There is also a quieter form of valuation pain — the low-LTV outcome. The deal goes through, but at 65% LTV instead of 80%. Or at a 15-year tenure instead of 25. The bank doesn’t reject; it just protects itself by reducing exposure. The borrower walks away thinking they got the loan. They got a loan — not the one they planned around.

Old Buildings and the OC/CC Problem

A particular technical trap, increasingly serious in 2025–26: properties without an Occupancy Certificate.

Following a now-widely-discussed line of Supreme Court directions, lenders across the spectrum have grown sharply more cautious about financing properties that lack OC/CC documentation, especially in completed buildings. This used to be an NBFC-flex zone — banks would decline, but NBFCs and HFCs could often structure something around it via LAP-style products at lower LTV and higher pricing. That window has narrowed materially.

The practical effect: a 25-year-old society building in central Mumbai or south Delhi, fully occupied, with residents who have been living there for decades, may today be effectively unfinanceable through a vanilla home loan if it cannot produce a clean OC. The flat is fine. The lifestyle is fine. The bank’s risk policy isn’t.

Sellers and brokers will often say “don’t worry, OC is just a formality, many flats here don’t have it.” For the lender, it is no longer a formality.

Technical Defects vs Lender Response

Technical defect

Typical bank response

Typical NBFC/HFC response

Valuation gap up to 5% of agreement value

Sanction at lower of two values; bridge the gap

Same; sometimes recognises stamp/registration in value

Valuation gap 10–15%

Lower LTV; some banks decline

Lower LTV at higher rate

Valuation gap above 20%

Usually decline

Lower LTV at significantly higher pricing

Major plan deviation (illegal floor, extension)

Decline

Decline

Minor plan deviation within tolerance

Sanction sometimes

Sanction

Building 30+ years old, OC clean

Lower LTV, shorter tenure

More flexible on tenure

Building 30+ years old, no OC

Mostly decline (post 2024 ruling)

Tightening; selective LAP

Narrow lane / poor access

Lower LTV

Lower LTV

Distress / low-liquidity locality

Decline or low LTV

Lower LTV at higher rate

🔍 Underwriter’s Note: Banks treat valuation as a number. NBFCs and HFCs treat valuation as a lever — they will often do a deal a bank declines, but by lowering LTV, raising the rate, and structuring the product differently. That flexibility is real, but it costs money. It is rarely the cheaper outcome.

The “Bank-Approved Project” Myth

If there is one phrase that has cost more Indian home buyers more money than any other, it is the one printed proudly on builder hoardings: Approved by all leading banks.

Borrowers read this and assume two things, both wrong.

They assume that bank-approved means legally clean. It doesn’t.

They assume that bank-approved means every bank will lend on it. It doesn’t.

What does “bank-approved project” actually mean?A bank-approved project is one where one or more lenders signed a project-level tie-up after reviewing the builder’s documents at a point in time. It is a marketing classification, not a permanent legal guarantee. It does not commit the bank to lending on every unit, does not bind any other bank, and does not survive subsequent litigation, plan deviation, or a change in the bank’s risk policy.

The phrase carries another quiet hazard. In a small number of cases — reported repeatedly in Indian financial press over the years — bank-approved has been a polite way of saying the builder has a commercial arrangement with the bank’s relationship manager, and individual unit-level due diligence is being skipped. When such projects later face litigation, RERA non-compliance, or completion delays, the individual legal opinion for your unit can still come back unclear, even though the project was, on paper, “approved.”

Here is the more accurate way to interpret builder marketing:

What the builder says

What it usually actually means

“Approved by all leading banks”

One or two banks have a project tie-up; others may decline

“RERA registered”

The project is registered. It does not validate every claim by the builder.

“Bank-funded project”

The builder has a construction finance loan, not a guarantee for buyer loans

“All approvals in place”

Approvals as of a certain date. Plan deviations during construction can invalidate this.

“Don’t worry about OC, it’ll come”

OC is at the discretion of the municipal authority. It may take years. Or never come.

The cleanest mental model: bank approval of a project is the bank’s opinion of the builder at one moment. Your loan is the bank’s opinion of your specific flat, your specific seller, and your specific paperwork. Trust your own legal opinion — or one you commission independently — far more than the framed certificates in the sales office.

🔍 What Banks Quietly Notice: Most builders have informal internal blacklists at banks — projects where past experience (delays, litigation, valuation issues, frequent borrower complaints) has made the credit team uncomfortable. These blacklists are rarely written down, never shared with borrowers, and don’t appear on any builder’s marketing material. The builder’s project may still be “approved by HDFC” while quietly disliked by three other lenders.

City-specific property risks that lenders flag during legal and technical verification across India’s major metros.

City-Wise Property Risk: What Lenders Actually Watch

India is not a single housing market, and lenders don’t apply a single set of rules. What gets rejected in Mumbai may get approved in Pune. What sails through in Bengaluru may stall in Chennai. Every city has its own profile of property risks that quietly dictate underwriting outcomes.

A condensed view of patterns we see repeatedly:

Mumbai

SRA rehab flats remain heavily restricted — a 10-year transfer lock-in, multiple court interventions, and recent scrutiny of SRA redevelopment projects have made banks especially conservative on units sourced through these channels. Old cooperative buildings without proper OC or with significant unauthorised extensions (lofts, mezzanines, illegal floors) face down-valuation or decline. Cessed buildings and structures slated for redevelopment carry their own enforcement risk for lenders, since the property’s future title and physical form are uncertain.

Delhi NCR

Banks “generally do not entertain” loans in unauthorised colonies. Lal Dora properties, GPA-only deals, and builder floors on partly regularised land routinely fail mainstream legal checks. Plan deviation — extra floors, conversions of residential to commercial, PG conversions — is a near-universal rejection trigger in Gurugram and Noida. The ZoneO and floodplain belts add another regulatory layer that lenders watch.

Bengaluru

The A-Khata vs B-Khata distinction is foundational. B-Khata properties are treated as regularisation-pending by banks; most decline outright, and even sympathetic lenders will impose tight conditions. Revenue sites (agricultural land not yet converted) need formal conversion to be financeable. Lake encroachment and Rajakaluve overlap concerns make some peri-urban layouts a hard no, regardless of how clean the seller’s paperwork looks.

Chennai

CMDA vs DTCP jurisdiction is the central question. Plot approved by DTCP where CMDA applies = legal defect. Unapproved layouts and patta inconsistencies in suburban panchayat areas regularly get marked not clear by panel lawyers. Even brand-new constructions on the wrong authority’s approval can fail the legal lens entirely.

Hyderabad

HMDA-approved + RERA-registered = lender-friendly. Gram Panchayat (GP) layouts on the urban fringe = lender-resistant. Map mismatches — flats let out as PG accommodation, residential plots used commercially — are flagged sharply by valuers and can collapse a sanction at disbursal stage.

Pune

Municipal approval and NA (non-agricultural) conversion are non-negotiable for most mainstream banks on plot/under-construction deals. PG conversions and unapproved redevelopment in central pockets (including some prime micromarkets) have drawn lender caution after high-profile irregularities.

Tier-2 and Tier-3 Cities

Documentation gaps dominate: incomplete mutations, outdated land records, unreleased prior mortgages, society resolution gaps. The pattern is consistent — local brokers and even sub-registrar offices consider deals “normal,” but centralised legal hubs at large banks reject the property after closer scrutiny. The friction isn’t fraud; it is simply slower civic record-keeping that creates a mismatch with the precision lenders now require.

The takeaway: ask your seller and broker city-specific questions, not just generic ones.“Is this A-Khata or B-Khata?” in Bengaluru is worth fifty hours of generic research.

📌 Visual placement: insert “India City-Wise Property Risk Heat Map” here. See visual concept brief at end of article.

How PSU Banks, Private Banks, and NBFCs See the Same Property Differently

One of the least-understood realities in Indian housing finance is that the same property file can get three different verdicts from three different categories of lenders. Borrowers often think of bank rejection as a final verdict on the property. It usually isn’t. It is the verdict of that one bank’s policy.

Defect type

PSU bank

Private bank

NBFC / HFC

Title defects, broken chain

Decline

Decline

Mostly decline

Active litigation

Decline

Decline

Decline

OC/CC missing

Mostly decline

Decline

Tightening; case-by-case

Major plan deviation

Decline

Decline

Decline

Building 30+ years old, OC clean

Lower LTV / shorter tenure

Sanction with conditions

More flexible

Building 30+ years old, no OC

Decline

Decline

Selective LAP

B-Khata / unapproved layout

Decline

Mostly decline

Selective at low LTV, higher rate

Valuation gap 15%+

Decline / lower LTV

Lower LTV

Lower LTV, higher rate

Self-employed + irregular property

Decline

Tight scrutiny

Most flexible

Resale flat with succession pending

Hold for legal cure

Hold for legal cure

Hold for legal cure

The pattern, simplified:

PSU banks are the most rule-bound. They lend cheapest, but they are slowest to deviate. They want a policy-perfect property and a policy-perfect borrower. Their internal audit and central legal hubs make it operationally difficult for branch staff to push deviations.

Private banks are more agile on borrower profile but still firm on core property hygiene. They will price risk and flex on conditions, but they will not lend on properties that look exposed to legal or municipal action.

NBFCs and HFCs are the most flexible — but their flexibility is not a free gift. It is paid for with lower LTVs, higher interest rates, and often a shift from a vanilla home loan to a LAP-structured or specialised “unapproved area” product. They will sometimes do what banks decline. They will rarely do what banks decline at bank pricing.

What this means in practice: if your loan gets rejected by one bank on property grounds, the question to ask is not “is my property unfinanceable?” The question is “is my property unfinanceable at standard home loan pricing, or unfinanceable everywhere?” The two are very different problems.

🔍 Underwriter’s Note: Inter-lender variance is real, but it has a limit. Title defects, active litigation, and clear illegality are universal nos. Approvals, OC issues, valuation gaps, and old-building cases are where lender choice can change the outcome. The skill is knowing which category your specific defect falls into — and that is the moment an experienced advisor saves you 3–6 months of failed reapplications.

Real Stories: How Strong Borrowers Lose Loans to Property Risk

Patterns are easier to internalise through cases. These are composites — anonymised representations of situations that recur across Indian lenders.

Case 1: 760 CIBIL, Sanction Letter in Hand, Killed by Legal

A salaried couple in Hyderabad, both IT professionals, joint applicants. CIBIL 760. Combined income ₹2.3 lakh per month. Sanction letter received within 11 working days for a flat in a mid-rise project from a “reputed local builder.” Token money paid: ₹2 lakh.

Three weeks later: legal verification flags a pending civil suit over the underlying land between the builder and an earlier landowner. The case is recent enough that the panel advocate marks the property not clear. Bank refuses disbursal.

The borrowers had assumed the sanction letter meant the deal was done. The builder’s salesperson — sincerely — had not known about the litigation; it was filed after the bank’s initial project tie-up. The buyers’ booking agreement had a refund clause, but only if the builder failed to deliver, not if the buyer’s loan failed. Recovery of the token took six months and a lawyer.

The lesson buried in this case: the sanction letter described the borrower as approved. The property was still under examination.

Case 2: Resale Flat with an Unreleased Old Mortgage

A mid-career professional in Mumbai bought a resale 2BHK in Andheri. Seller appeared respectable. Society had loans on multiple flats. Buyer’s broker insisted “all papers are clear.”

Bank legal verification surfaced an old, unreleased mortgage from a since-merged HFC — never formally satisfied because the seller’s family had moved on after closing the loan and assumed the bank would do the rest. The bank wanted a NOC from the original lender (or its successor) before disbursing. The successor entity took eight weeks to locate the file, and another four weeks to issue the NOC.

The buyer lost two months. The seller, by then, was visibly impatient. Registration almost collapsed twice.

The lesson:“all papers clear” is broker language. A title can carry a perfectly clean appearance and still have an unreleased charge no one has bothered to extinguish.

Case 3: Valuation Came In ₹14 Lakh Lower

An IT manager in Pune, with a strong profile, agreed ₹95 lakh for a flat in an overpriced micro-market. The bank’s empanelled valuer assessed fair market value at ₹81 lakh — a 14.7% gap.

The bank’s policy: lend on the lower of the two. At 80% LTV, the borrower was now eligible for ₹64.8 lakh instead of the ₹76 lakh he had budgeted for. He had to either renegotiate with the seller, walk away from the deal, or arrange an additional ₹11.2 lakh in 12 days.

He renegotiated. The seller, who had multiple buyers, refused. He walked away. The token money clause favoured the builder. He absorbed a ₹3.5 lakh loss.

The lesson: in overheated micro-markets, the bank’s valuation is sometimes the cheapest piece of due diligence you can buy — if you commission a private valuation before paying token rather than after.

Case 4: Unauthorised Floor Discovered During Technical

A first-time buyer in Delhi NCR was attracted to a top-floor unit in a builder-floor property because it was offered at a 12% discount. The “discount” was the top floor — which the technical valuer noted was constructed beyond the sanctioned plan.

Mainstream banks declined immediately. Even NBFCs offering specialised products declined, citing demolition risk under municipal action. The buyer’s booking amount of ₹4 lakh became disputed; recovery took over a year.

The lesson: when a price looks too good, the unauthorised square footage is almost always the explanation. Banks don’t fund square footage that doesn’t legally exist.

Case 5: Repeat Rejections — and Bureau Damage

A self-employed borrower in Lucknow applied for a home loan five times across four months, on the same property — a partially regularised plot in a colony with documentation gaps. He kept hearing “try another bank, sir,” and kept doing so.

Each application generated a hard enquiry on his bureau. By the fourth attempt, his CIBIL had dropped 22 points — not catastrophic, but enough that future lenders saw a string of recent rejections and grew cautious. Meanwhile, the underlying property issue — the documentation gap — was the same every time, and every panel lawyer was reaching the same conclusion.

The lesson: if the property is the problem, throwing more lenders at it doesn’t help. Fix the property issue or change the property before applying again. Otherwise, you’re just damaging your credit profile while the underlying problem stays untouched.

Borrower Myths That Quietly Increase Property Risk

A small collection of beliefs that look harmless but cost real money. These show up almost every week in conversations with borrowers in panic mode.

Myth: “Sanction letter means my loan is done.” Reality: The sanction letter is conditional on legal and technical clearance of the property. Many sanctions are reversed at disbursal stage.

Myth: “Token money is fully refundable if my loan is rejected.” Reality: Most booking agreements protect the seller, not the buyer. Refund clauses are usually limited to seller-side default. Read the booking form before paying.

Myth: “Bank-approved project = legally guaranteed.” Reality: Bank approval reflects the bank’s view of the project at one point. It does not bind other banks, and it doesn’t guarantee approval for your specific unit.

Myth: “If one bank rejects, I’ll just apply to another.” Reality: If the issue is the property, all lenders will reach similar conclusions on the core defects. Each application creates a bureau enquiry. You damage your credit profile without solving the property problem.

Myth: “OC is just a formality. Everyone in the building lives without it.” Reality: Post 2024 Supreme Court direction, OC is no longer a paperwork formality for lenders. Many old buildings without OC have become effectively unfinanceable.

Myth: “Famous builder = safe property.” Reality: Famous builders run projects that face delays, RERA non-compliance, and ongoing litigation just like smaller ones. The brand reduces risk on intent. It does not eliminate risk on documents.

Myth: “RERA registration = all clear.” Reality: RERA registration is one filter, not a complete one. It does not validate every builder claim. Read the RERA filing carefully — the project details, completion dates, complaints, and amendments are often more revealing than the certificate itself.

Myth: “The bank’s lawyer is on my side.” Reality: The panel advocate is the bank’s lawyer. Their job is to protect the bank’s collateral, not to advise you. If you want a lawyer working for you, you have to commission your own.

Myth: “My banker said everything will be fine.” Reality: Front-line bankers are sales-incentivised on disbursals, not on legal verification. They often genuinely don’t know what the legal hub will flag. The branch is not where the rejection decision lives.

Myth: “If property is registrable, it must be financeable.” Reality: Registrable ≠ financeable. The sub-registrar’s job is to record transactions. The lender’s job is to underwrite collateral. Their criteria are different.

Myth: “Resale flats are always safer because the building is complete.” Reality: Resale flats carry a different — often heavier — risk profile: succession gaps, unreleased mortgages, society conveyance issues, and OC questions on older buildings.

Home Loan Property Verification Checklist: What to Confirm Before Token

This is the single most valuable section in this article. If you only act on one part, act on this one.

The cost of every problem described above collapses to near-zero if you check these items before you pay any meaningful money. After you pay token, your bargaining power evaporates and your sunk cost emotion takes over.

Title and Ownership

Last 13 to 30 years of sale deeds / mother deed available

Encumbrance Certificate (EC) for the relevant period, clean

Mutation in current seller’s name in revenue/society records

For inherited property: succession certificate or registered will or relinquishment deeds in place

All joint owners willing to sign — including spouses where law requires

No outstanding unreleased mortgages or charges on title

Approvals and Compliance

Sanctioned plan available, matching the actual built structure

Commencement Certificate (CC) for under-construction

Occupancy Certificate (OC) for completed buildings — confirmed covers your specific wing/unit

RERA registration number verified directly on the state RERA portal (not just the builder’s certificate)

For plots: NA conversion done, layout approved by the correct authority (CMDA / DTCP / BDA / HMDA / etc.)

Hyderabad-specific: HMDA-approved (preferably not just GP-approved)

No unauthorised floors, illegal extensions, or use-change

Society and Operational

Society share certificate in seller’s name

Society conveyance / deemed conveyance executed (Mumbai specifically)

Society NOC available for transfer

No pending maintenance dues, no pending society litigation

Property tax paid up to date

Utility bills in seller’s name and up to date

Builder / Project (For Under-Construction)

RERA project number checked directly on the state RERA portal

Builder’s prior project track record (delivery history, complaints)

Approval letters from the actual sanctioning authority — not just the builder’s marketing

Construction-finance bank, if any, not the same as the bank you’re approaching for buyer loan (avoidable conflict)

Sale agreement clauses on refund of token money in case loan is rejected — negotiate in writing

Valuation

Indicative valuation done — ideally informally through a known valuer or banker — before finalising agreement value

Comparable transactions in the building / locality validated (sub-registrar records, online portals as starting point)

Reality-checked against the agreement value; gaps over 10% are a warning

Documentation Trail

Buyer’s own copy of all property documents (not just the builder’s marketing brochure)

Independent lawyer’s opinion commissioned before paying token, not after

Copy of all approvals and certificates, dated and verified

If any of these items can’t be cleanly produced, the right move is to delay token payment, not to pay first and verify later. The negotiation power exists on one side of token; the desperation exists on the other.

📥 Lead magnet placement: insert “Pre-Token Property Approval Checklist (PDF)” download CTA here. See lead magnet brief at end of article.

If Your Home Loan Is Already Rejected Due to Property: The Recovery Playbook

For readers in panic mode — already paid token, already received the rejection — the situation is rarely as binary as the bank’s response makes it sound. Here is the operational sequence to work through.

Step 1: Find Out Why, Specifically

The single most useful thing you can do is get the exact reason in writing. Front-line staff will say things like “legal not clear” or “property issue” without elaborating. Push politely but firmly for the specific clause or finding.

Ask:

Was it a title issue, an approval issue, or a valuation issue?

Can you share the legal opinion (or at least its key observation)?

Was it a borrower issue, a property issue, or both?

If it’s a property issue, you also need to know which lens failed — title, approvals, technical, valuation — because the recovery path is completely different in each case.

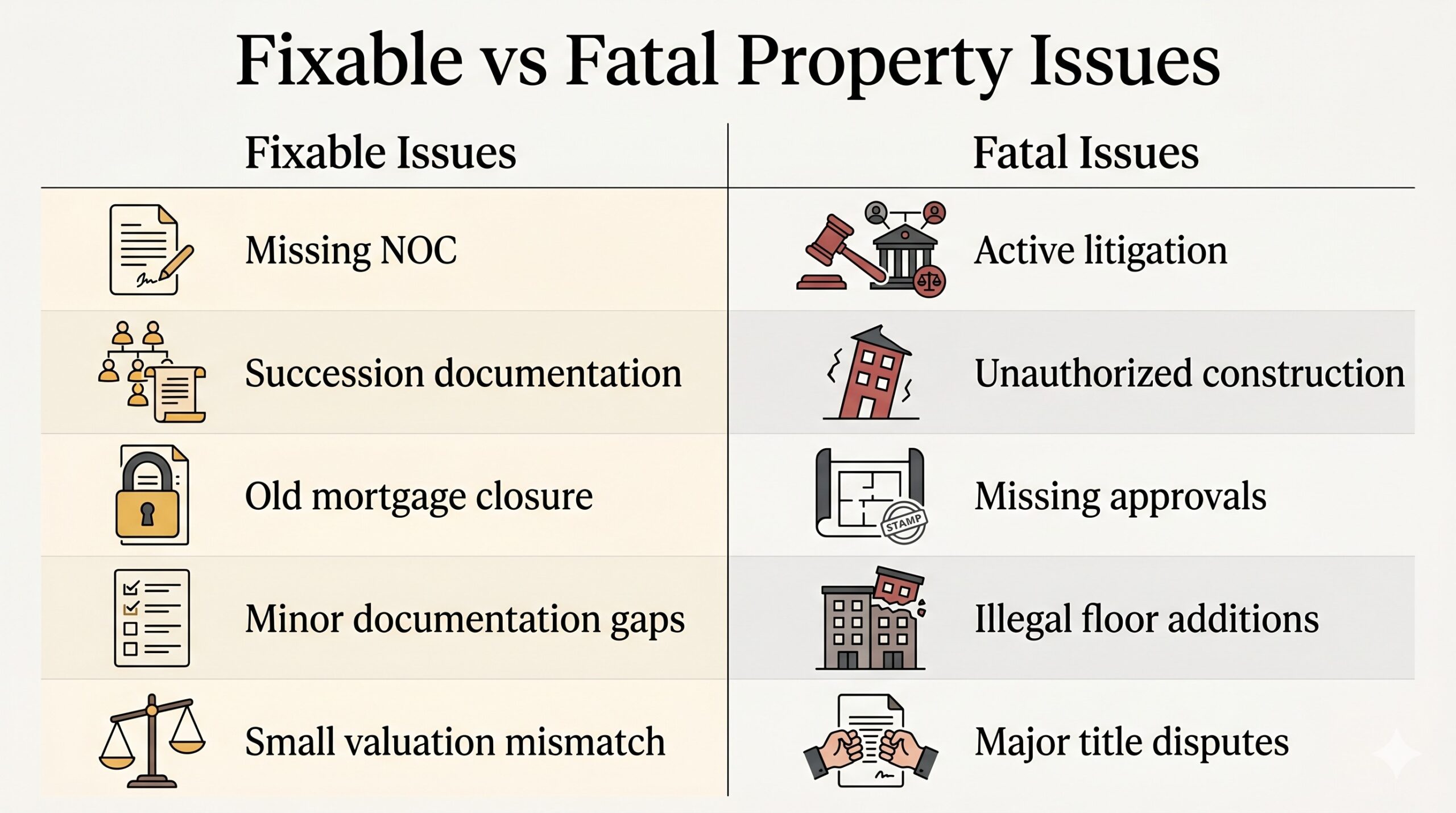

Step 2: Classify — Fatal or Fixable

Use this framing:

Knowing whether a property defect is fixable or fatal determines your next move — cure the issue and reapply, or walk away and protect your credit.

Type of issue

Typical outcome

Active litigation on title

Fatal — change property

Major plan deviation, unauthorised construction

Fatal — change property

Wrong jurisdiction approval

Fatal in most cases

Unauthorised colony

Fatal for mainstream lenders; possibly NBFC at cost

OC/CC missing (completed building, post 2024)

Tightening — limited NBFC options at lower LTV

Unreleased prior mortgage

Fixable — get NOC from prior lender

Succession not done

Fixable — legal work over weeks

Missing NOCs, minor docs

Fixable — collect and resubmit

Valuation gap

Fixable in some cases — renegotiate price, bridge with savings, or change lender

Be honest with yourself. The cost of pursuing a fatal problem is far greater than the cost of accepting it and changing course.

Step 3: For Fixable Issues — Fix Them, Then Reapply

Get the specific defect addressed: NOC from prior lender, succession papers, missing approvals.

Wait until the fix is documented, not just promised.

Then reapply — ideally to a lender with stronger appetite for that specific property type (e.g., HFCs for older buildings, banks for newer projects). Before reapplying, review your home loan eligibility to maximise your chances.

Don’t make multiple parallel applications. The bureau enquiry damage compounds.

Step 4: For Valuation Issues — Three Real Options

Option A: Renegotiate with the seller using the bank’s valuation as evidence. Some sellers will move; many won’t.

Option B: Bridge the gap from savings or other sources. Only sensible if the underlying valuation is genuinely defensible and you have margin to spare.

Option C: Approach a lender that may value differently (some NBFCs, some private banks) or that recognises stamp duty/registration in their funded amount. You may get a slightly better outcome, but expect a higher rate.

Don’t try to fund the gap with a personal loan and call the problem solved. The math rarely works.

Step 5: For Fatal Property Issues — Walk Away, Salvage What You Can

If the property is genuinely fatal — active litigation, unauthorised construction, completely missing approvals — the right move is almost always to walk away and absorb the token loss as the cost of avoiding a far larger loss.

The harder problem is recovering the booking amount. This depends entirely on the language of your booking agreement. Some clauses allow refund if the loan is not sanctioned; many do not. If your agreement is unfavourable, a written communication to the builder, citing inability to obtain finance and requesting refund or unit-change, is the starting point. Legal action is the next step if needed. Most builders will negotiate before they litigate.

Step 6: Protect Your Credit Profile

A property-led rejection does not directly damage your CIBIL score. But the hard enquiry generated by your application stays on your bureau for 12–24 months. Multiple applications, multiple enquiries — a pattern visible to future lenders.

Avoid the temptation to “try another bank quickly.” If the property is the problem, the next bank will reach the same conclusion. Either fix the property or change the property before applying again.

🔍 Underwriter’s Note: When a file is declined for property reasons, central credit teams sometimes mark it internally with a category code. If you reapply to a sister entity (e.g., the bank’s HFC arm or an affiliated NBFC), that code can travel with the file. The polite “try another bank” suggestion isn’t always a clean fresh start — it depends on the relationship between the two entities.

Persona-Specific Property Risks

Different buyers carry different blind spots. A short, honest snapshot:

The First-Time Salaried Buyer

You are likely focused on the EMI, the sanction letter, and the move-in date. Your single biggest risk is paying token money before any independent legal verification. You will trust the builder more than you should and read the booking form less carefully than you should. The protective move: spend ₹15,000–25,000 on an independent lawyer’s review before you pay anything. It is the cheapest insurance you will ever buy.

The High-Income Urban Buyer

You are time-poor and confident of clearance. Your blind spot is buying premium projects in semi-regularised areas, or relying on a wealth manager who is not a property lawyer. The protective move: ask not “will I get a loan?” but “what is the specific approval status of this property in the eyes of three different lenders?” If a project’s loan eligibility is sensitive to which bank you choose, that is information you need before token.

The Self-Employed Borrower

You are used to documentation friction on your own side. The blind spot: you may compromise on property legality to get a flexible lender, or buy in semi-regularised areas because the price is right. The protective move: be especially careful about the combination of imperfect documentation on both sides — your income docs and the property docs. Lenders that flex on one rarely flex on both.

The Investor Buyer

You optimise for yield and appreciation. Your blind spot: under-construction projects, pre-launch deals, builder-bank tie-up offers with subvention schemes. The protective move: read the RERA filing and the construction finance details, not just the brochure. Bookings in delayed projects carry risk no spreadsheet captures.

The Resale Property Buyer

You assume that a completed, occupied building means it’s safe. The blind spot: old building OC issues, society conveyance gaps, unreleased prior mortgages, succession incompleteness. The protective move: ask for the OC, society share certificate, and EC before you discuss price. If the seller hesitates on producing these, the deal already has a problem.

What This All Comes Back To

A home loan in India is not a single approval. It is the simultaneous approval of two files — yours and the property’s. Most borrowers spend 90% of their preparation effort on their own file, and almost no effort on the property’s. The math of where rejections actually happen is the inverse.

The property has its own credit committee, its own panel lawyers, its own valuers, its own escalation matrix, its own grading system, and its own grounds for rejection. None of that is visible from the outside. From the borrower’s seat, it just looks like “the bank said no” — vague, frustrating, expensive.

The shift in mindset that protects you isn’t complicated. It is this:

Before you ask “will the bank approve me?”, ask “will the bank approve this property?”

Verify the property like a lender would. Commission your own legal opinion before token. Get an indicative valuation before agreement value is finalised. Read the RERA filing directly. Confirm OC, plan, and authority approvals. Understand which specific local risks apply to your city’s housing stock. Negotiate a real refund clause into the booking form. And then — only then — start thinking about which bank to approach.

Most home loan rejections in India are not rejections of the borrower. They are rejections of the asset. The borrowers who learn this early stop losing money on token forfeitures and lawyer fees, and start treating property selection as the first underwriting decision rather than an afterthought.

If you take only one thing from this article, let it be this:

Approval is not where the home loan journey starts. Property verification is.

The good news is that property risk is one of the most preventable financial mistakes a home buyer in India can make — if you check the right things before you commit money, in the right order, with the right independent eyes on it. The borrowers who get hurt are almost always the ones who treated the property as a romance and the loan as a transaction. The borrowers who stay safe do exactly the opposite.

You now know what banks look at, what they quietly notice, which issues are fatal and which are fixable, and how lender categories flex differently on the same property. You know what to demand from your seller, your builder, and your lawyer — and what to refuse to do until those answers are in your hands.

That’s not a guarantee against every problem. But it is the difference between walking into a home loan as a passive applicant and walking in as someone who already thinks like the underwriter on the other side of the desk.

That shift is what protects your money.

Frequently Asked Questions

Can a home loan be rejected after the sanction letter is issued?

Yes — far more often than borrowers realise. The sanction letter is an in-principle approval, conditional on the property clearing legal and technical verification. If the panel advocate’s opinion comes back not clear, or the valuation lands well below the agreement value, the file can be downsized, conditioned, or declined at disbursal stage. Inside the lender, this is treated as a property-side decline, not a borrower-side decline — but the borrower experiences it as one.

What does “bank-approved project” mean for home loan approval?

It means one or more banks have done a project-level tie-up after reviewing the builder’s documents at a point in time. It does not guarantee approval for every individual unit, it does not bind other banks, and it does not survive subsequent litigation or non-compliance. Always commission your own legal verification on the specific unit you are buying.

Why is my bank’s valuation lower than my agreement price?

The empanelled valuer reports a fair market value based on comparable transactions, building age, locality liquidity, and construction quality — not on what the buyer has negotiated. A 5–10% gap is common in active markets. A gap above 15% is the valuer quietly telling the bank that the micro-market is overheated, the property has weak resale liquidity, or there are technical issues being paid a premium to ignore. The credit team reads it the same way.

Can I get a home loan on a property without an Occupancy Certificate?

Increasingly difficult. Following Supreme Court direction tightening lender obligations around OC/CC, many banks now decline OC-missing properties, and even NBFCs and HFCs have narrowed their flexibility. Older buildings without OC may need a regularisation route or a specialised LAP product at lower LTV and higher rates.

Can another bank approve my loan if one bank rejected the property?

Sometimes — but only when the first rejection was policy-driven (that bank’s LTV minimums, age cutoffs, locality stance). When the rejection is defect-driven — title issues, missing approvals, active litigation, plan deviations — every other lender’s legal panel reaches the same conclusion. The skill is knowing which category your specific rejection falls into before you waste applications and bureau enquiries on the wrong lenders.

Will my CIBIL be affected if my home loan is rejected due to property issues?

The rejection itself does not directly affect your CIBIL score. However, every loan application generates a hard enquiry that stays on your bureau for 12–24 months. Multiple applications across a short window create a visible pattern that future lenders treat as a caution signal.

Is RERA registration enough to ensure my loan gets approved?

No. RERA registration is one filter, not a complete one — and lenders treat it that way. Panel advocates read the RERA filing for what the builder has disclosed (delivery dates, complaints, amendments, financial extensions), not just the certificate. Verify the project’s filing directly on the state RERA portal yourself, and commission an independent legal opinion regardless. RERA registration is the starting point of due diligence, not the conclusion.

What’s the difference between OC and CC for a home loan?

A Commencement Certificate (CC) is permission to start construction. An Occupancy Certificate (OC) confirms that the completed building complies with the sanctioned plan and is fit for occupation. Banks typically want OC for completed buildings before disbursing. CC alone is insufficient for a completed structure.

Can I get my token money back if the bank rejects my home loan?

It depends almost entirely on the booking agreement — and most are written to protect the seller, not the buyer. Refund clauses are usually limited to seller-side default. The protective move is to negotiate a loan rejection refund clause in writing before paying token. After payment, recovery depends on the agreement language and the builder’s willingness to settle. In practice, most builders will negotiate before they litigate — especially if you have a paper trail showing the rejection was driven by their property’s documentation, not your profile.

Should I apply to multiple banks at the same time to be safe?

No. Multiple simultaneous applications generate multiple hard enquiries on your bureau and create a pattern of “loan shopping” that future lenders read negatively. Apply to one well-chosen lender at a time. If property is the problem, fix or change the property before reapplying — not the lender.

FOIR in home loan is the single most important number that determines how much loan you’ll get — yet most borrowers never check it. If you’re planning to take a home loan in India, understanding your Fixed Obligation to Income Ratio could be the difference between financial freedom and years of stress. This guide breaks…

A 6-minute read that explains what banks actually evaluate — and what you can do about it. ☕ Let’s start with something that might feel uncomfortably familiar… You’ve done everything “right.” Your salary is decent.Your CIBIL score looks strong.You’ve planned your finances carefully. You apply for a home loan… and then: “We regret to inform…

Most people over-borrow. This guide shows your safe limit. Last Updated: April 2026 ⚡ Quick Answer: How Much Home Loan Can I Afford in India? If you’re wondering how much home loan you can afford in India, the honest answer isn’t what your bank tells you — it’s what your lifestyle can sustain. Before you…

A borrower-protection guide written from the underwriter’s side of the table. Reading Time: 8 Minutes Editor’s Note: This article combines practical housing-finance experience, underwriting principles and borrower affordability frameworks commonly used across Banks, NBFCs and HFCs in India. About this guide. Written by a housing finance professional with 20+ years across credit, risk, operations, and…