Bank vs NBFC vs HFC: Which Home Loan Lender Is Actually Right for You in India?

A borrower-protection guide written from the underwriter’s side of the table.

Reading Time: 8 Minutes

About this guide. Written by a housing finance professional with 20+ years across credit, risk, operations, and strategy in Indian housing finance. Built on first-hand experience of how Indian home loan files are actually underwritten — across banks, NBFCs, and HFCs — and on current RBI/NHB regulatory frameworks as of May 2026. Read more about the editor →

Choosing between a Bank vs NBFC vs HFC home loan is one of the most consequential decisions an Indian borrower will make. This guide breaks down the real differences in how banks, NBFCs and housing finance companies (HFCs) underwrite your file — covering FOIR in home loans, home loan underwriting, and a practical home loan lender comparison — so you can match the right lender to your profile.

Last Updated: 20 May 2026

Quick Compass: If You Are… → Usually Best Fit

A starting orientation before we go deeper. Treat this as a compass, not an answer.

| If you are… | Usually the best first call |

|---|---|

| A salaried professional with stable income, CIBIL 750+, formal employer | A large public sector or top private bank |

| Self-employed with healthy business but modest declared ITR | A specialised HFC or a quality NBFC with surrogate income programs |

| A small business owner, trader, or cash-heavy borrower | An NBFC or affordable-housing HFC — but with a strict FOIR cap |

| A first-time buyer in an affordable housing project | A PSU bank linked to PMAY or state schemes, or a housing-focused HFC |

| Borderline CIBIL (650–720), thin file, or recently rejected | A specialised HFC first; NBFC second; never a desperation application |

| High-ticket borrower with ESOPs, bonus-heavy income, luxury property | Top private bank with a marquee HFC as a backup |

But the real answer is more nuanced than a table can carry. Lender fit is rarely about the lender’s brand. It is about how that specific lender’s underwriting team will read your file — and whether the EMI they sanction will quietly compound stress over twenty years, or genuinely fit your life.

Key Takeaways

- ✓ Banks usually offer lower rates but stricter approvals

- ✓ NBFCs offer greater flexibility but often higher pricing

- ✓ HFCs are often strong options for self-employed and affordable housing borrowers

- ✓ Approval does not equal affordability

- ✓ Choose lender fit, not lender type

Table of Contents

- Introduction: Two Borrowers, Same Income, Different Lives

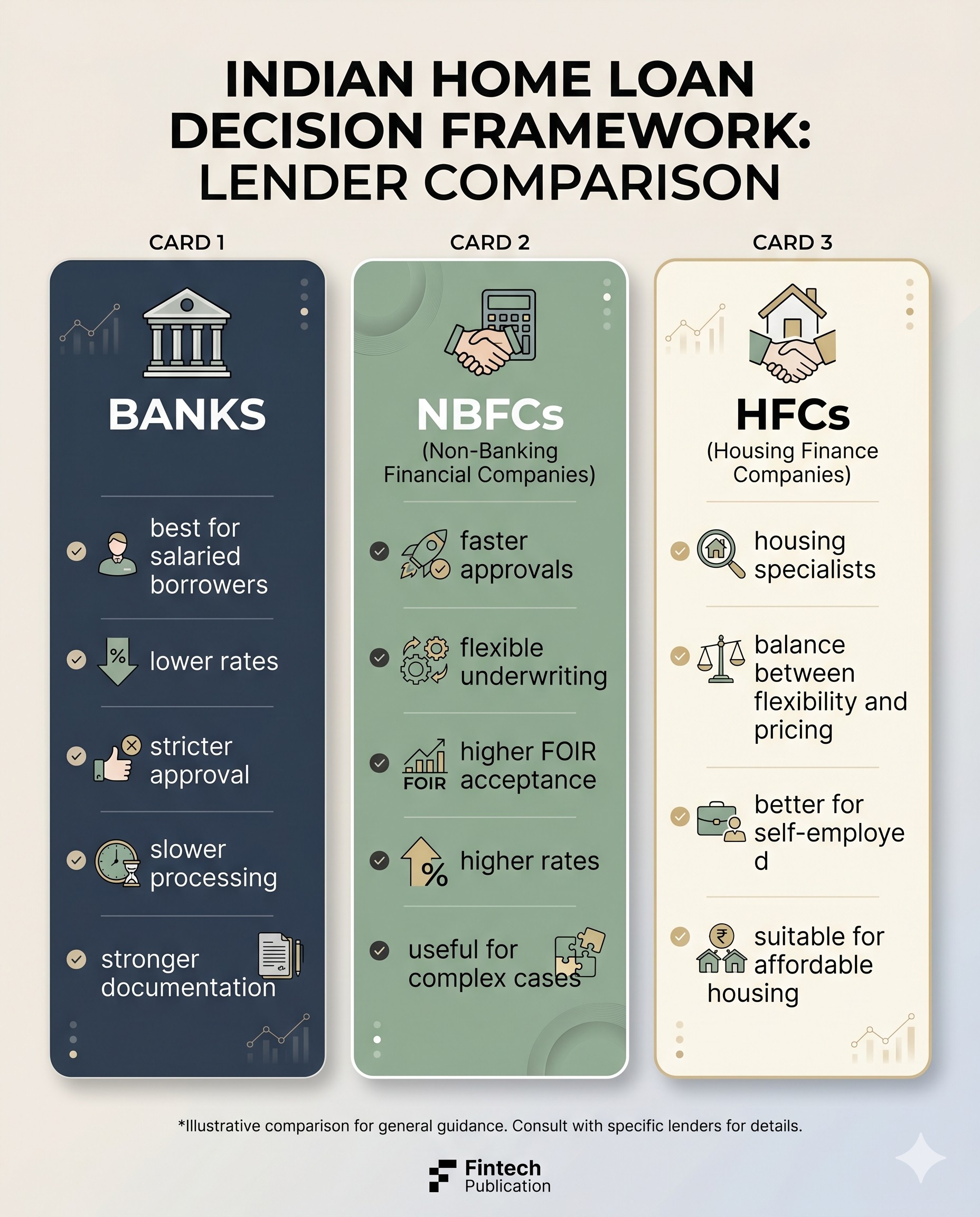

- Section 1: Banks, NBFCs and HFCs — Beyond the Textbook Definitions

- Section 2: How Home Loan Lenders Actually Judge You

- Section 3: Bank vs NBFC vs HFC — The Real Comparison

- Section 4: Which Lender Fits Your Profile?

- Section 5: The Most Dangerous Home Loan Mistake — Approval ≠ Affordability

- Section 6: Real Indian Borrower Stories

- Section 7: So… Which Lender Should You Actually Choose?

- Section 8: Red Flags Before You Sign Any Home Loan

- Section 9: The Final Verdict

- Section 10: Frequently Asked Questions

- Section 11: Key Takeaways

Introduction: Two Borrowers, Same Income, Different Lives

Two engineers. Same salary, ₹1.6 lakh net per month. Same city. Same kind of flat in roughly the same price band. They both walked into the home-buying process around the same time.

One went to a public sector bank. After three weeks of documentation, slower processing, and a polite but firm reality check on his eligibility, the bank sanctioned ₹65 lakh. His EMI sits at about ₹55,000 — comfortable, with room left over for a sick parent, a child’s school fees, and the kind of monthly chaos no spreadsheet captures.

The other one was in a hurry. The builder had a “limited offer”. An NBFC sanctioned ₹82 lakh in 72 hours. His EMI is closer to ₹70,000. On paper, his approval looked stronger. Bigger sanction. Faster turnaround. More flat for the money.

Two years in, the second borrower has stopped his SIPs, dipped into his emergency fund twice, and quietly resents the fact that the bonus he counted on this year didn’t come through. He isn’t in default. He looks fine from the outside. He just isn’t living the life he thought a home loan was supposed to fund.

Approval is not the same as affordability. Two lenders looking at the same borrower can produce wildly different sanction amounts — and the larger sanction is not always the better outcome.

The choice between a bank, an NBFC, and an HFC is not really a choice between three institutional categories. It is a choice between three different philosophies of risk, three different reading styles of your financial file, and three different long-term consequences for your household. The lender you pick decides not just your interest rate, but how much breathing room your life gets to keep.

That is what this guide is actually about.

Section 1: Banks, NBFCs and HFCs — Beyond the Textbook Definitions

Most articles will tell you a bank is a deposit-taking institution regulated by the RBI, an NBFC is a non-deposit-taking financial company also regulated by the RBI, and an HFC is a housing-focused NBFC that was earlier under the NHB. All of that is true. None of it tells you what you actually need to know.

What matters is how each one behaves when your file lands on an underwriter’s desk.

Banks: built to protect deposits, not to maximise your sanction

A bank takes public deposits. Every loan it approves is, in a sense, lending out somebody else’s savings. That single fact shapes everything — the conservative FOIR limits, the preference for formal salaried borrowers, the slower processing, the deeper documentation, the rigid property checks. A bank’s underwriter is paid to keep the NPA ratio low. Your file is one of thousands; the system is engineered to filter out risk, not to find creative ways to approve you.

When the profile fits, a bank gives you the cheapest long-term cost, repo-linked rate transmission, and an institutional rhythm that survives recessions. When the profile is off, a bank says no — politely, and often without explaining why.

NBFCs: built to price risk, not to avoid it

An NBFC cannot accept public demand deposits. It funds itself from banks, bonds, and capital markets — at a cost higher than what banks pay for deposits. To stay profitable, an NBFC has to lend at a higher spread. To grow, it has to take on borrowers banks turn away.

This is not a flaw in the model. It is the model. An NBFC’s underwriter doesn’t ask “is this risky?” — they ask “can this risk be priced?” That is why NBFCs will stretch your FOIR, accept a 680 CIBIL, work with two years of ITR instead of three, and process the whole thing in 48 hours. The flexibility is real. So is the cost — and the borrower who confuses the two pays for that confusion every month for the next twenty years.

HFCs: built around the home, not just around the loan

A Housing Finance Company is now treated under RBI’s regulatory umbrella as a category of NBFC, after the 2021 Master Directions and subsequent harmonisation. By rule, an HFC must keep at least 60% of its assets in housing finance, with a meaningful share lent directly to individuals. That sector-specific constraint shapes its DNA.

An HFC underwriter typically knows local property markets better than a bank’s centralised team, has deeper exposure to specific micro-segments — affordable housing, Tier-2 self-employed borrowers, plot-plus-construction loans — and is comfortable with files banks find awkward. Some marquee HFCs feel almost bank-like in conservatism; some affordable-housing HFCs feel almost NBFC-like in flexibility. They are not a uniform category. Read each one on its own terms.

What the regulatory shift actually means for you

Since the RBI took over HFC supervision and harmonised the framework — including the RBI (Housing Finance Companies) Directions, 2025 and the April 2026 amendments that allow HFCs to include audited quarterly profits in their owned-fund calculations — the gap between HFCs and NBFCs has narrowed structurally. They share capital adequacy norms (15% minimum), liquidity rules, and the same RBI-mandated disclosures. The HFC of 2026 is not the loosely supervised entity of a decade ago. That is good news for borrower safety.

Two more things worth keeping in mind. From October 2024, lenders — including banks, NBFCs, and HFCs — must issue a Key Fact Statement (KFS) for retail and MSME loans, disclosing the all-in Annual Percentage Rate (APR), every charge, and the amortisation schedule. This single document is the most powerful borrower-protection tool to come out of recent regulation. And the RBI ban on foreclosure and prepayment charges on floating-rate home loans applies across banks, NBFCs, and HFCs — though fixed-rate loans can still carry exit fees. We will come back to both of these when they actually matter.

Official references: Lending and disclosure norms for banks, NBFCs and HFCs are governed by the Reserve Bank of India (RBI) and the National Housing Bank (NHB). Always cross-check current rules on these official portals before signing.

Section 2: How Home Loan Lenders Actually Judge You

Borrowers tend to assume lenders look at one thing: the salary slip. The truth is that there are roughly six levers an underwriter pulls, and the weight given to each one is what separates banks from NBFCs from HFCs.

FOIR: the single number that decides your real eligibility

What is FOIR? Fixed Obligation to Income Ratio (FOIR) is the percentage of your monthly income committed to existing EMIs plus the proposed new EMI. Lenders use it to test home loan affordability. A FOIR of 40–50% is generally safe; above 55% is stretched; above 65% is dangerous regardless of approval.

The RBI’s own guidance suggests banks typically assume 55–60% of monthly disposable income can go towards EMIs. But there’s a quiet trap inside that number — some lenders use gross income, others use net, and the difference can be ₹30,000 a month on a senior-manager salary.

Here’s how the three categories typically treat FOIR: Banks are comfortable up to 40–50% on most prime profiles, with some going to 55% for very high-income borrowers with strong compensating factors. NBFCs routinely stretch to 55–65%, especially in Tier-2/3 markets or for self-employed files. HFCs show a wide range — conservative HFCs behave like banks; affordable-housing HFCs behave like NBFCs.

What the brochures don’t tell you is that FOIR has stress zones, not just an upper limit.

The FOIR Stress Zones

| FOIR Band | What it really means |

|---|---|

| Under 35% | Comfortable. Room for school fees, parents, emergencies, life. |

| 35–45% | Workable. Most households can sustain this without lifestyle compression. |

| 45–55% | Stretched. One income shock, one medical event, and you’re in trouble. |

| 55–65% | Dangerous. You are technically approved and structurally exposed. |

| Above 65% | Avoid. Even if a lender offers it, walk away. |

When you hear that an NBFC has approved you at a FOIR your bank refused — that is not necessarily a compliment to your finances. It may simply mean someone is willing to price the risk your bank refused to take.

CIBIL: the score behind the score

A CIBIL score above 750 generally gets you the best pricing at banks. Between 700 and 750, you are still in the conversation but the rate may be slightly higher. Between 650 and 700, banks become cautious; NBFCs and HFCs become interested. Below 650, your options narrow sharply and the cost rises.

But two things go unsaid. First, the bureau also reads your credit behaviour pattern — how often you apply, how recently you closed an unsecured loan, whether your credit card utilisation runs above 70%. A score of 760 with five hard enquiries in the last six months may look weaker than a 720 with a clean recent history. Second, multiple loan applications across lenders, especially in a short window, leave bureau footprints that drag the score down further. The same anxiety that pushes borrowers to apply everywhere is the very behaviour that makes approval harder.

LTV: how much skin lenders want you to have in the game

The RBI sets clear caps on Loan-to-Value (LTV) Ratio: up to ₹30 lakh loan amount — maximum 90% LTV; ₹30 lakh to ₹75 lakh — maximum 80% LTV; above ₹75 lakh — maximum 75% LTV. These slabs apply across banks, NBFCs and HFCs. The difference is what each lender does within the cap. Banks tend to value the property conservatively, which effectively pulls the LTV down.

NBFCs and HFCs, especially in affordable segments, may use a higher valuation that pushes the LTV close to the regulatory ceiling. A 90% LTV on a 50% FOIR is a borrower with almost no buffer for anything — a job change, a medical bill, a slow business quarter. The numbers add up on paper. They don’t add up in life.

Property quality: the silent rejection factor

This is the one most borrowers never see coming. You can have a CIBIL of 800, a perfect salary slip, and a clean FOIR — and still get rejected because the property has issues the lender’s legal and technical team flagged. The flat is in a building marked as NPA by the builder’s own bank. The plot has Waqf board complications. The independent house has no approved plan copy. The society lacks occupancy certificate. The builder is blacklisted by that specific lender. None of these will show up in your credit profile. All of them can end the conversation.

Banks tend to be strictest here. HFCs, with deeper local property knowledge, sometimes find ways through that banks won’t touch. NBFCs vary widely. Always — always — ask for a verbal property clearance from the lender before paying token money to the builder.

Employer category: an invisible underwriting filter

Banks maintain internal employer category lists. PSU, Tier-1 IT, top MNCs, established corporates — Category A. Mid-tier listed companies — Category B. Smaller unlisted firms, regional businesses, recent startups — Category C or below. Your salary slip may say the same number, but the employer behind it changes the rate you get, the FOIR you’re allowed, and sometimes whether you’re allowed in at all. NBFCs and HFCs are usually more comfortable with non-marquee employers, which is part of why a banking rejection at a smaller firm often becomes an HFC approval.

Self-employed assessment: where the categories diverge most sharply

For salaried borrowers, the three lender types look fairly similar. For self-employed borrowers, they look like three different industries.

A bank, in most cases, reads your last three years of ITR, calculates an average net profit, and works backwards to eligibility. Heavy depreciation, legitimate tax deductions, and conservative book-keeping all reduce the income the bank sees — even though your actual cash flow may be twice that.

NBFCs and HFCs use surrogate income models. The Banking Surrogate assesses you based on 12 months of bank statement turnover and average balance — useful for professionals and businesses with strong banking but modest ITR. The GST Surrogate uses your monthly GST filings to estimate real turnover, useful for traders, manufacturers, and service businesses with formal GST footprint. The Cash-flow Surrogate combines banking, GST, and sometimes vendor/customer references to build a holistic income picture.

A doctor whose ITR shows ₹18 lakh but whose clinic revenue is ₹36 lakh — the bank will assess on ₹18 lakh, the HFC on close to ₹30 lakh. The eligibility difference can easily be ₹40 lakh of sanctioned amount. That flexibility is genuinely valuable. It is also dangerous when used to maximise loan size rather than match real affordability.

A traditional bank reads a 60% FOIR as an impending default. An NBFC reads it as a priceable risk. Both are correct from their own balance-sheet perspective. Neither of them is sitting in your living room when the EMI hits the account every month. That part is yours.

Underwriter’s Desk

Section 3: Bank vs NBFC vs HFC Home Loan — The Real Comparison

A genuine Bank vs NBFC vs HFC home loan comparison has to go deeper than a rate chart. Most comparison articles run a table on interest rates and processing fees and stop there. Those numbers matter. They are not where the actual differences live.

The four-line summary

| Banks | NBFCs | HFCs | |

|---|---|---|---|

| Rate (2026) | 8.35–9.25% | 8.75–11.50% | 8.50–10.50% |

| FOIR appetite | 40–50% | 50–65% | 45–60% |

| CIBIL needed | 750+ | 650+ | 680+ |

| Best for | Stable salaried | Speed, surrogate income | Housing specialists |

The full comparison

| Dimension | Banks | NBFCs | HFCs |

|---|---|---|---|

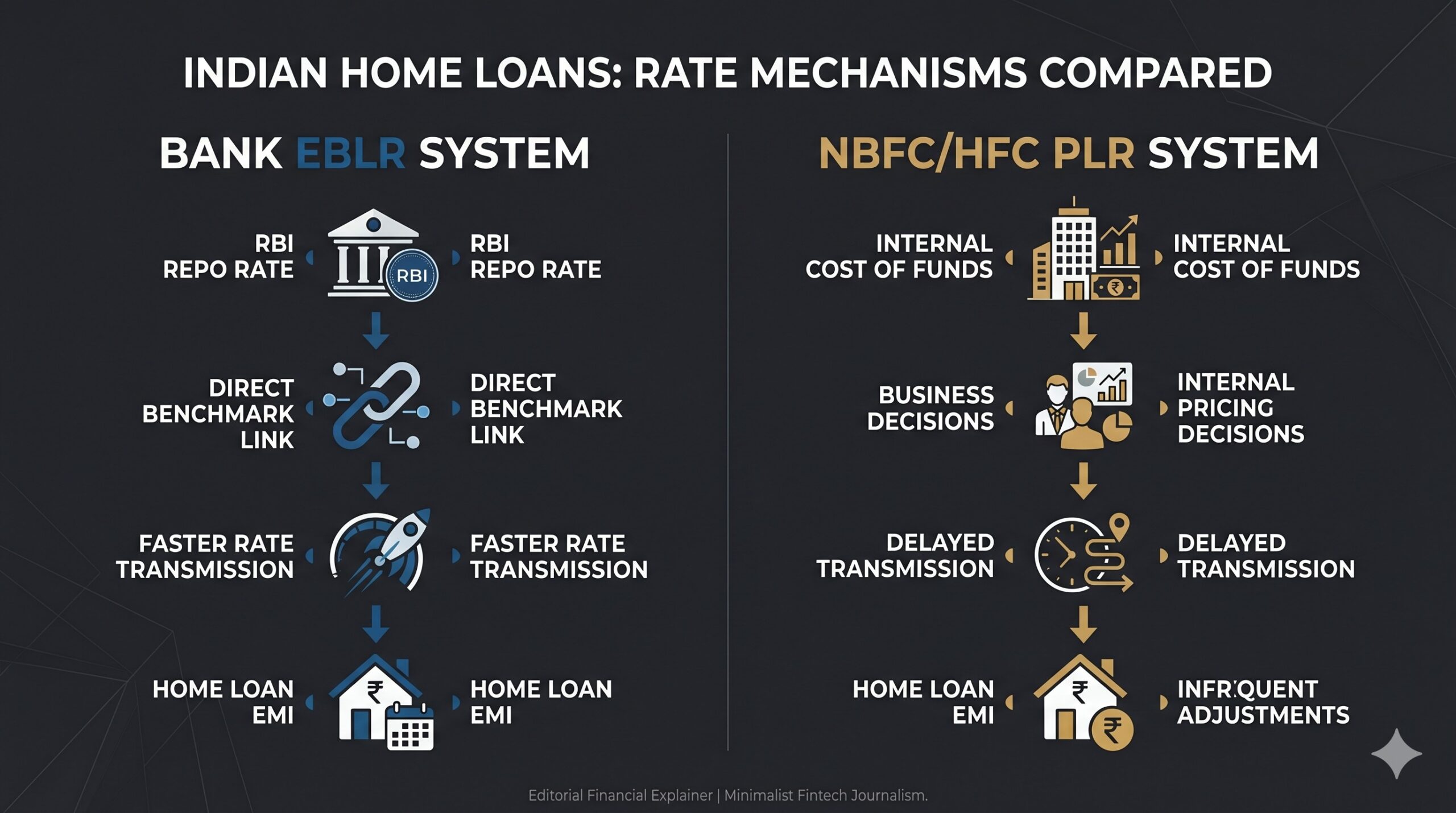

| Rate transmission | EBLR / repo-linked; fast cuts and fast hikes | Internal PLR; slower transmission, both ways | Internal PLR; behaviour close to NBFCs |

| Self-employed assessment | ITR-based, conservative | Surrogate income; flexible | Surrogate-friendly; housing-specialist |

| Property risk appetite | Lowest — strict legal/technical | Moderate; varies by lender | Often highest in housing segments |

| Processing TAT | 7–15 days for most cases | 24–72 hours common | 3–7 days typical |

| Documentation burden | Heaviest | Lightest | Moderate |

| Sales aggression | Lowest | Highest | Moderate to high |

| Foreclosure on floating loans | RBI-banned, no charges | RBI-banned, no charges | RBI-banned, no charges |

| Foreclosure on fixed loans | Charges allowed, disclosed | Often higher charges | Charges allowed |

| Long-term cost | Lowest if profile fits | Highest unless refinanced | Mid-range |

| Refinancing flexibility | Easiest target lender for HLBT | Easiest source for HLBT | Both source and target |

EBLR vs PLR: Why Rate Transmission Matters to You

Banks (EBLR — External Benchmark Lending Rate): Rates are linked to the RBI repo rate. When the RBI cuts rates, your EMI can drop within 3 months. Rate hikes also pass through quickly.

NBFCs & HFCs (PLR — Prime Lending Rate): Rates are set internally. Cuts are slower to pass through to borrowers. Hikes may also move differently. Less predictability for long-tenure loans.

Over a 20-year home loan, the difference in rate transmission can affect your total interest outgo by several lakhs.

A few observations the table can’t carry. Rate transmission is asymmetric in your favour at banks. When the repo rate drops, your EBLR-linked bank loan reprices fairly quickly — usually within a quarter. An NBFC’s PLR-linked loan often lags. This matters less in a stable rate environment and a lot in a falling one.

A 48-hour NBFC approval feels like a gift when the builder is pressuring you. It is also exactly the moment you have least time to think. The bank’s slower process is, in some sense, a structural cooling-off period — and many borrowers later wish they had taken it.

The “no foreclosure charges” rule is more nuanced than the headlines suggest. RBI banned foreclosure and prepayment charges on floating-rate home loans across banks, NBFCs, and HFCs. Fixed-rate home loans — and certain hybrid products — are still allowed to carry exit fees. Read your KFS. The APR section will show every charge that applies.

HFCs are not a single category. A large public-sector-backed HFC behaves more like a bank. An affordable-housing HFC behaves more like an NBFC. A mid-tier HFC sits somewhere in between. Always evaluate the specific HFC, not the category label.

Section 4: Which Lender Fits Your Profile?

The right question is not “which lender is best?” It is “which lender’s underwriting model reads my file most accurately and prices my risk most fairly?”

Salaried professional, formal employer, stable income

A bank, almost always. The rate advantage compounds significantly over 15–20 years. The conservative FOIR will protect you from yourself when the builder offers a slightly bigger flat. If the bank’s eligibility number feels too small, that is a signal worth listening to — not bypassing.

Where an HFC may make sense: when the property is in a Tier-2 or Tier-3 location where banks are restrictive, or when the project is one that local HFCs know better than national banks. Where an NBFC rarely makes sense for this profile: you are paying a premium for flexibility you don’t need.

Self-employed professional with healthy business but modest ITR

The classic surrogate-income case. A specialised HFC with a strong professional segment is often the sweet spot — they understand cash flow, they accept banking and GST surrogates, and they price closer to bank rates than NBFCs do. A quality NBFC works as a second choice, especially if you need speed or your file has any complications.

A bank is worth trying first, but only if you have time. Banks will sometimes consider professionals more generously than the standard ITR rule suggests, but only if you walk in with audited financials, CA-certified income, and a strong banking relationship.

Small business owner, trader, mixed cash and digital income

Be honest with yourself. If your ITR is meaningfully below your actual cash flow, a bank conversation will be frustrating. Either spend a year cleaning up your books and applying later, or accept that an HFC or NBFC is the realistic path now.

The discipline here is non-negotiable: cap your FOIR at 50%, even if the NBFC offers you 60%. Take the smaller loan. Buy the slightly smaller flat. Plan a balance transfer to a bank in 24–36 months once your CIBIL strengthens and your business banking is two years cleaner.

First-time buyer in an affordable housing project

A PSU bank linked to PMAY or state housing schemes is almost always the best first call. The subsidies, the priority-sector treatment, the lower rates — all compound in your favour. A housing-focused HFC with strong scheme integration is a close second.

The single biggest mistake in this segment: maxing out both 90% LTV and 50% FOIR. That is two warning lights at once. Either bring more own funds, or take a smaller loan.

Borderline CIBIL (650–720) borrower

Do not apply everywhere. Each rejection drags the score lower and makes the next approval harder. Pick one specialised HFC that explicitly underwrites in this band, apply there only, and use the next 12 months to bring the CIBIL above 750. Then balance-transfer to a bank.

If you must apply somewhere fast — for token money or a builder deadline — go directly to a single HFC or NBFC known for this segment. Skip the banks. They will reject, and the enquiry will hurt you.

High-ticket borrower, complex income, premium property

A top private bank that already has your salary account or wealth relationship is your primary call. Their pricing power on a ₹2 crore+ loan is real, and the relationship matters. A marquee HFC works as a backup, especially if the property has any features the bank’s policy is uncomfortable with. An NBFC is a niche solution — only for very specific structuring needs.

Section 5: The Most Dangerous Home Loan Mistake — Approval ≠ Affordability

This is the section that matters more than any rate table.

A sanction letter is a lender’s statement that they are willing to lend you a certain amount at a certain price. It is not a financial planner’s recommendation. It is not a statement that this loan fits your life. It is not a stress test of what happens to your household if your bonus doesn’t come through, your spouse takes a career break, or your parents need long-term care.

Lenders price for their risk — the probability that you will default to the point where it shows up on their books. Your life can deteriorate in many ways before that point. You can stop your SIPs. You can skip vacations. You can cut your child’s extracurriculars. You can quietly drain the emergency fund. You can argue with your spouse every month about money. None of that shows up in the lender’s NPA report. All of it shows up in your life.

The 20-30-40 framework is a useful anchor — not because it is a regulation, but because it reflects what financially healthy households actually look like: 20% own-funds contribution as down payment (minimum); 30% cap on total EMIs as percentage of net monthly income; 40% target allocation to living expenses, savings, and emergency reserves. Most lenders will sanction loans that take you well past 30% on the EMI line. That is not a bug in their system — it is a feature, because they are optimising for sanction volume, not your long-term financial health. The discipline of staying near 30% has to come from you.

The approval may look affordable today. Life rarely stays static for 20 years.

Inflation is the part borrowers most consistently forget. School fees rise. Healthcare costs rise faster than headline inflation. Your child’s tuition at age six is not what their college fees will be at age sixteen. Your parents’ medical needs at sixty are not what they will be at seventy-five. A FOIR that feels comfortable today, on a salary that has been growing 8% a year, can feel suffocating in a year when the increment is 3% and the bonus is zero. Many borrowers don’t realise this until the EMI actually starts.

Section 6: Real Indian Borrower Stories

These are composite cases drawn from common patterns in housing finance — anonymised, realistic, and built around real underwriting outcomes you see in the market.

Case 1: The Bengaluru IT couple who took the bigger loan

Profile. Combined net income ₹2.4 lakh per month. Existing car loan EMI ₹30,000. CIBIL 780 and 765. Looking at a ₹1.1 crore apartment in a primary Bengaluru micro-market with clear title and a known developer.

Bank outcome. A large private bank ran the file and came back with a sanction of ₹78 lakh — they capped the EMI at ₹68,000, keeping FOIR at around 41% of net income after accounting for the car loan. The underwriter was comfortable but not generous. The rate offered was 8.65%, repo-linked. Processing took 12 days.

NBFC outcome. An NBFC, contacted the same week, sanctioned ₹88 lakh in 72 hours. EMI ₹78,000. FOIR around 45%. Rate 9.40%. Faster, larger, more expensive.

What they did. They took the NBFC offer. The flat was a better unit, the builder discount was time-bound, and the EMI felt manageable on paper. They closed the car loan from savings to bring FOIR down.

What happened. Eighteen months in, the wife took a six-month sabbatical that turned into a planned career switch — eight months of single income. The EMI didn’t change. The emergency fund did. They paused SIPs for ten months, took a small personal loan to bridge a medical event for an aging parent, and watched their household financial slack disappear.

The lesson. Both lenders correctly assessed the file at the time. The NBFC was not predatory. The bank was not being conservative for the sake of it. The difference was the buffer — the ₹10,000 of monthly headroom the bank’s sanction would have preserved, which became precisely the cushion the household needed eighteen months later. The decision that felt like a win at signing became the source of two years of financial tension. The smarter path would have been to take the bank’s smaller sanction and either bring more own funds, or accept the slightly smaller flat.

A strong dual income looks bulletproof on a sanction sheet. It is a fragile structure in real life. Career breaks, parental health events, and the simple chemistry of two professionals in their thirties making different choices — all of these reduce real household income in ways no underwriting model anticipates. The right FOIR is not the one your lender allows. It is the one that survives one of your two incomes being temporarily out.

Underwriter’s Desk

Case 2: The Tier-2 doctor whose ITR didn’t tell the truth

Profile. Single applicant. Clinic revenue ₹3.2 lakh per month based on banking and patient billing. ITR shows ₹19 lakh annual net income after legitimate practice expenses, equipment depreciation, and staff costs. Existing vehicle loan EMI ₹22,000. CIBIL 738. Looking at a ₹82 lakh ready-to-move 3BHK in a Tier-2 city.

Bank outcome. Two public sector banks and one private bank assessed the file. The PSU banks worked off ITR — average monthly income calculated at around ₹1.58 lakh net — and offered sanctions of ₹42–48 lakh at rates around 8.85%. The private bank, after he submitted CA-certified income and 24 months of clinic banking, went to ₹54 lakh at 8.95%. None of them was willing to use surrogate income as the primary basis.

HFC outcome. A specialised HFC with a professionals’ programme used banking surrogate (12-month average clinic account balance and turnover) and got to an assessed income of about ₹2.65 lakh per month. Sanction ₹68 lakh at 9.35%. EMI around ₹58,000. FOIR around 30%. Processing took 6 days.

NBFC outcome. An NBFC offered ₹72 lakh at 10.10%, with a higher FOIR cushion. Faster turnaround. More expensive.

What he did. Took the HFC offer. Bought the flat with ₹14 lakh of own funds plus the ₹68 lakh loan, kept his clinic working capital intact, and registered with a clear plan to balance-transfer to a bank in 30 months once his CIBIL crossed 770 and his banking surrogate strengthened further.

What happened. Twenty-eight months later, he initiated a Home Loan Balance Transfer to a private bank at 8.55%. Saved approximately ₹38 lakh over the remaining tenure. The HFC’s slightly higher initial rate was, in retrospect, the cost of accessing realistic eligibility when his ITR alone wouldn’t have got him there.

The lesson. For self-employed professionals with modest declared income, the surrogate-friendly HFC is often genuinely the best lender — and the right exit plan is built in from day one. The rate premium is the price of access; the balance transfer is how you eventually capture the bank rate without having needed it on day one.

Three lighter sketches

The Pune shop owner with seasonal income. Garments business, average ₹85,000 monthly cash flow, ITR understates this by half. CIBIL 692, no existing EMIs. Property: ₹38 lakh house in a peripheral township. PSU bank: cautious decline, citing income inadequacy. NBFC: approved at ₹28 lakh, 10.85% rate, fast. Affordable-housing HFC: approved at ₹31 lakh, 9.75% rate, with PMAY linkage that brought effective cost lower. Best fit: the HFC. The NBFC was faster but the HFC’s scheme integration mattered more than speed for a borrower with no income shock absorber.

The 28-year-old first-time buyer in an NCR affordable project. Salaried, ₹68,000 net, no existing obligations. CIBIL 742. Property: ₹32 lakh in an approved affordable housing project. PSU bank offered 90% LTV at 8.45% with PMAY benefit. HFC offered the same LTV at 8.85%. Best fit: the PSU bank. Cheaper, scheme-linked, no real reason to go elsewhere — and the discipline of capping the loan at 80% LTV would have been wiser still.

The high-FOIR salaried borrower with a recent CIBIL dip. ₹1.3 lakh net, ₹35,000 existing EMI from a personal loan that’s still running, CIBIL dropped from 781 to 698 after a missed payment six months ago. Bank: declined. Two NBFCs: approved at high FOIR (62%) at rates above 10%.

Best fit: none of them, yet. The right answer was to close the personal loan first, let the CIBIL recover for nine months, and then approach a bank or HFC. The borrower instead took the NBFC offer, paid the penalty for nine months of higher EMI, and is now stuck with a balance-transfer plan that won’t fully crystallise for another two years.

Section 7: So… Which Lender Should You Actually Choose?

After all the frameworks, the practical decision usually comes down to a small set of filters.

The Borrower–Lender Fit Matrix

| Your situation | First call | Second option | Avoid |

|---|---|---|---|

| Prime salaried, clean profile | Bank | HFC | Premium NBFC pricing |

| Self-employed professional, healthy banking | HFC (surrogate) | NBFC | Bank, unless time-rich |

| Self-employed, weak ITR, cash-heavy | NBFC or affordable HFC | Bank (after cleanup) | Maxing FOIR for higher loan |

| First-time buyer, affordable segment | PSU bank with scheme | HFC | NBFC at higher rate |

| Borderline CIBIL, recent issues | One specialised HFC | None | Multiple applications |

| High-ticket, complex income | Top private bank | Marquee HFC | NBFC unless structured |

The deeper filter underneath this matrix is a single test. Run the EMI through three stress scenarios before you sign:

Income shock test. Assume one income in the household disappears for six months. Does the EMI still get paid from existing resources?

Expense shock test. Assume school fees, medical costs, and household inflation rise 15% next year. Does the EMI still leave you with monthly savings?

Rate shock test. For floating-rate loans, assume the rate rises 100 bps. What does the new EMI look like, and can you sustain it?

If any of these tests fail, the lender’s approval doesn’t matter. The loan is too big for your life.

Section 8: Red Flags Before You Sign Any Home Loan

A short checklist — designed to make you pause at the right moments.

Warning signs in the offer itself

- FOIR above 55%, even if the lender is comfortable with it

- LTV at 90% combined with FOIR above 45%

- A “no-questions-asked” approval on a file that another lender just rejected

- Rate quoted as “starting from X%” without your specific rate in writing

- Pressure to sign before you’ve read the KFS

- Processing fee above 1.5% of loan amount (NBFCs often quote 2%+; this is negotiable)

- Sanction letter that doesn’t clearly state the property the loan is against

- Insurance products being bundled without explicit opt-out

Warning signs in your own situation

- Token money already paid and you’re now applying for the loan — this is the opposite of how it should go

- Multiple loan applications in the last 90 days

- Existing unsecured loan EMIs above 15% of net income

- Less than three months of expenses in emergency savings, after the down payment

- A spouse or co-applicant who is not enthusiastic about the purchase

- The deciding emotion is “I don’t want to lose this flat” rather than “this loan fits our life”

Questions to ask before signing, in writing

- What is the all-in APR including processing, valuation, legal, and insurance? (KFS will show this; insist on seeing it.)

- Is the rate floating, fixed, or hybrid? When does it reset?

- What are the foreclosure and prepayment charges for this specific rate type?

- What is the property valuation amount used to calculate LTV?

- What employer category am I being assessed in, and how does that affect the rate?

- If I want to balance-transfer in 24 months, are there any contractual restrictions?

- What is the exact list of charges that will be debited at disbursement?

A lender who can’t answer these clearly, in writing, is not the lender you want to spend the next two decades with.

Section 9: The Final Verdict

Home loans in India are sold as a product. They are lived as a relationship — a twenty-year financial commitment that shapes the rhythm of every month of your household’s life. The lender you choose is not just a counterparty. They are, in a sense, a co-investor in your life decisions, with rights over your largest asset and a quiet influence on every other financial choice you make for the next two decades.

Banks, NBFCs, and HFCs are not better or worse than each other in any absolute sense. They are differently engineered for different kinds of borrowers. A bank is excellent for the borrower whose file fits its model — and frustrating for the borrower whose file doesn’t. An NBFC is genuinely valuable for the borrower who needs speed, flexibility, or surrogate-income recognition — and expensive for the borrower who didn’t need any of those things. An HFC, when well chosen, is often the sweet spot for the borrower who falls between the rigid bank model and the more transactional NBFC approach.

The best lender is not the one willing to lend you the most money. It is the one that helps you build your home without quietly damaging your financial future.

What the choice ultimately comes down to is not a category, but a question. Does this specific lender’s offer, on this specific property, at this specific FOIR, leave your life intact? Does it leave room for the parents, the children, the bonuses that don’t come, the medical bills that do, the SIPs that are quietly building your retirement, the small monthly margin that is what financial freedom actually feels like?

Ultimately, the right Bank vs NBFC vs HFC home loan decision is the one that fits your income profile, FOIR headroom and property — not the lender with the flashiest rate. Use the home loan lender comparison, underwriting signals and affordability checks in this guide to choose the lender that protects your household for the next two decades.

Section 10: Frequently Asked Questions

1. What is the main difference between a bank, an NBFC, and an HFC for home loans?

In a Bank vs NBFC vs HFC home loan comparison, the core difference is regulatory and structural. Banks are RBI-regulated, deposit-taking institutions offering the lowest interest rates with strict eligibility. NBFCs cannot accept public demand deposits, fund themselves at higher costs, and lend at higher rates with more flexible underwriting and faster processing. HFCs are housing-focused NBFCs that must keep at least 60% of assets in housing finance; they sit between banks and pure NBFCs in pricing, flexibility, and housing-segment specialisation.

2. Is it safe to take a home loan from an NBFC or HFC?

Yes. Both are regulated by the RBI under the NBFC and HFC Directions, with capital adequacy norms of 15%, liquidity coverage requirements, and the same Key Fact Statement disclosures banks must provide. The 2025 RBI HFC Directions and April 2026 amendments have further harmonised regulation. The borrower’s risk is not the lender’s instability — it is the higher rate and FOIR if the loan is not refinanced over time.

3. What is FOIR in a home loan?

Fixed Obligation to Income Ratio (FOIR) is the percentage of your monthly income committed to existing EMIs plus the proposed new EMI. Lenders use it to test home loan affordability. A FOIR of 40–50% is generally safe; above 55% is stretched; above 65% is dangerous regardless of approval.

4. What is a safe FOIR for a home loan?

For most Indian households, a FOIR of 35–45% leaves enough room for school fees, parental support, healthcare, and emergency savings. Some lenders will sanction loans up to 60% FOIR, but that approval level removes nearly all the financial slack from your monthly life.

5. What CIBIL score do I need for a home loan in 2026?

A CIBIL score of 750+ gets you the best pricing at most banks. 700–750 keeps you in the conversation but the rate may be slightly higher. 650–700 is the band where NBFCs and HFCs become more relevant than banks. Below 650, your options narrow and the cost rises sharply.

6. Why was my home loan rejected despite a good CIBIL score?

Rejections at high CIBIL are usually driven by one of three things: high FOIR from existing obligations, employer category issues, or property-specific problems (NPA-marked property, missing approvals, builder blacklisted by the lender, title issues). A strong score does not override these.

7. Can self-employed borrowers get home loans without traditional ITR-based eligibility?

Yes. NBFCs and HFCs offer surrogate income programmes — Banking Surrogate (uses 12 months of bank statements), GST Surrogate (uses GST filings), and combinations. These programmes assess real cash flow rather than declared net profit, and often produce significantly higher eligibility than ITR-based bank assessment.

8. Should I take an NBFC loan if a bank rejected me?

When weighing a Bank vs NBFC vs HFC home loan after a rejection, the answer depends on why the bank said no. Choose an NBFC over a bank when: you need surrogate income recognition (banking or GST-based); your CIBIL is in the 650–720 band; you need a sanction in under 7 days; your property has features banks typically refuse; or you have a clear balance-transfer plan to a bank within 24–36 months. If the rejection was due to genuinely unaffordable EMI relative to your income, no NBFC approval will change that underlying reality.

9. Can I transfer my home loan from an NBFC or HFC to a bank later?

Yes. Home Loan Balance Transfer (HLBT) is a standard product. Most borrowers can move from NBFCs/HFCs to banks after 12–24 months of clean repayment, provided their CIBIL has improved, the property documents are clean, and the rate differential justifies the transfer cost. Many borrowers structure their initial NBFC/HFC loan with this exit explicitly planned.

10. Are there foreclosure charges on home loans in India?

For floating-rate home loans, the RBI has banned foreclosure and prepayment charges across banks, NBFCs, and HFCs. For fixed-rate and hybrid loans, charges are still permitted but must be disclosed in the Key Fact Statement (KFS). The RBI also caps LTV at 90% for loans up to ₹30 lakh, 80% between ₹30–75 lakh, and 75% above ₹75 lakh — applicable across all lender categories.

11. What is the 20-30-40 rule for home loans?

A financial planning framework: at least 20% as down payment from own funds, total EMIs capped at 30% of net monthly income, and 40% of income preserved for living expenses, savings, and emergencies. It is more conservative than what lenders will sanction, and that is precisely why it works.

12. How is the Key Fact Statement (KFS) useful to borrowers?

The October 2024 RBI mandate requires lenders to issue a KFS showing the all-in Annual Percentage Rate (APR) — including processing fees, valuation charges, legal fees, and insurance — along with the full amortisation schedule. It is the most powerful tool for comparing real costs across lenders, because it strips out the headline-rate marketing and exposes total cost.

13. Are NBFC and HFC interest rates negotiable?

Yes, more than borrowers usually realise. Especially on processing fees (often 1.5–2% but negotiable to 0.5–1%), and sometimes on rate by 25–50 basis points if you have a competing offer in hand. Always get at least two offers in writing before negotiating.

14. Can I get a home loan with irregular or seasonal income?

Often yes, through HFC or NBFC surrogate programmes that assess turnover, banking averages, or GST history. Banks find this harder. The eligibility may be lower than your headline cash flow suggests, and the rate higher than a bank’s, but the access is real.

15. What is the biggest mistake first-time home loan borrowers make?

Chasing the maximum sanction. The lender’s sanction is the ceiling, not the recommendation. Most first-time borrowers would be financially healthier with a loan that is 15–20% smaller than what they are approved for. The flat is forever; the EMI is monthly. Get the EMI right first.

Section 11: Key Takeaways

Here is the quick recap of this Bank vs NBFC vs HFC home loan guide, distilled into the points that protect your household the most:

- The best lender is not the one with the lowest advertised rate or the highest approval. It is the one whose underwriting reads your file accurately and prices your risk fairly.

- Approval is not affordability. A sanction letter is a lender’s view of their risk, not a planner’s view of your life.

- FOIR matters more than rate over a 20-year tenure. A 45% FOIR at 9% will hurt less than a 60% FOIR at 8.5%.

- Banks reward formal, stable, well-documented borrowers with the lowest long-term cost.

- NBFCs and HFCs are not lenders of last resort. They are lenders of different specialisation — fast, flexible, surrogate-friendly — and the right choice for genuine non-standard files.

- HFCs are not a uniform category. Read each one individually.

- The KFS, mandatory since October 2024, is the single most important document to read before signing.

- Foreclosure charges are banned on floating-rate loans across banks, NBFCs, and HFCs. Fixed-rate loans may still carry them.

- For self-employed borrowers with modest ITR, the HFC surrogate-income path is often genuinely the best route — and a planned balance transfer to a bank is the right exit.

- The 20-30-40 rule is not a regulation. It is a description of what financially healthy households look like.

- Three stress tests — income shock, expense shock, rate shock — should be run before signing any sanction letter.

- A larger sanction is not a better outcome. It is more loan, more EMI, less monthly slack, and more financial fragility.

Who Should Read This Guide?

This guide is built for borrowers who want to understand the real mechanics of the home loan decision — not just the headline rate. It is especially relevant for:

- First-time home buyers who are navigating the lender landscape for the first time and want to make an informed decision rather than a reactive one.

- Self-employed borrowers whose ITR understates their actual income and who need to understand which lender types are actually equipped to assess their file accurately.

- Salaried professionals comparing lenders who want to understand why their bank’s conservative sanction may be the right number — and not just the lowest offer.

- Borrowers rejected by banks who are considering NBFCs or HFCs and want to understand the trade-offs before they sign.

- Households worried about EMI affordability who want a framework — not just a rate comparison — to assess whether a loan truly fits their life over a 15–20 year horizon.

About the Editor

Author is a housing finance professional with 20+ years of experience across credit, risk, operations, audit, compliance, and strategy in Indian housing finance and NBFC lending. He has worked across location-level, regional, and national leadership roles within India’s housing finance industry, with deep operational exposure to underwriting, credit policy, retail risk assessment, and the regulatory frameworks set by the RBI and NHB.

He writes HomeLoansIndia.co.in’s borrower-education editorial — built on operational underwriting experience, not marketing material.

LinkedIn · About the editor

Editorial Trust Statement

HomeLoansIndia.co.in is an independent borrower-education and housing-finance insights platform. Editorial decisions are independent and not influenced by lenders or financial institutions. Our content is based on operational housing-finance experience and publicly available RBI/NHB regulatory frameworks. Our objective is to help Indian borrowers make better, more confident home loan decisions — not to route them to any specific lender.

Last reviewed: May 2026

Disclaimer: The borrower scenarios in this guide are composite cases reflecting common underwriting patterns. Specific interest rates, eligibility outcomes, processing timelines, and lender behaviours vary by individual profile, property type, and prevailing market conditions, and are illustrative as of May 2026. This article is educational and not personalised financial advice. Regulatory frameworks, lender policies, and interest rates are subject to change. Always consult your sanction letter, the Key Fact Statement (KFS), and a qualified financial advisor before signing any home loan agreement.